Navigating Scope 3 and Value Chain Sustainability: A Guide for Private Companies

Gary Gao, CEM, PMP, SEA

Senior Manager

Gary has over 10 years of experience in the energy and sustainability space. He excels in developing holistic energy and sustainability strategy, engaging stakeholders and guiding clients through their sustainability journey. His breadth of experience is diverse and expansive from working with many Fortune 500 clients to being educated in multidisciplinary fields of engineering, environmental policies, and business.

These days, more large publicly traded companies are either voluntarily setting ambitious carbon reduction targets are being mandated to monitor scope 3 emissions and consider a broad number of value chain sustainability issues.

But why should private companies care about these issues?

As part of the value chains and therefore scope 3 emissions of these larger companies, smaller companies will be expected to share their sustainability metrics and emissions data with the larger companies they transport products for, supply and give services to, and partner with. Private companies can gain a competitive edge, manage risks, and ensure they are complying with any future regulations by implementing a strong ESG program and becoming sustainability leaders in their industry.

This blog explores why private companies should care about scope 3 and value chain sustainability and how businesses can navigate the challenges and opportunities they face in measuring, managing, and reducing their environmental and social impacts.

Understanding Scope 3 and Value Chain Sustainability

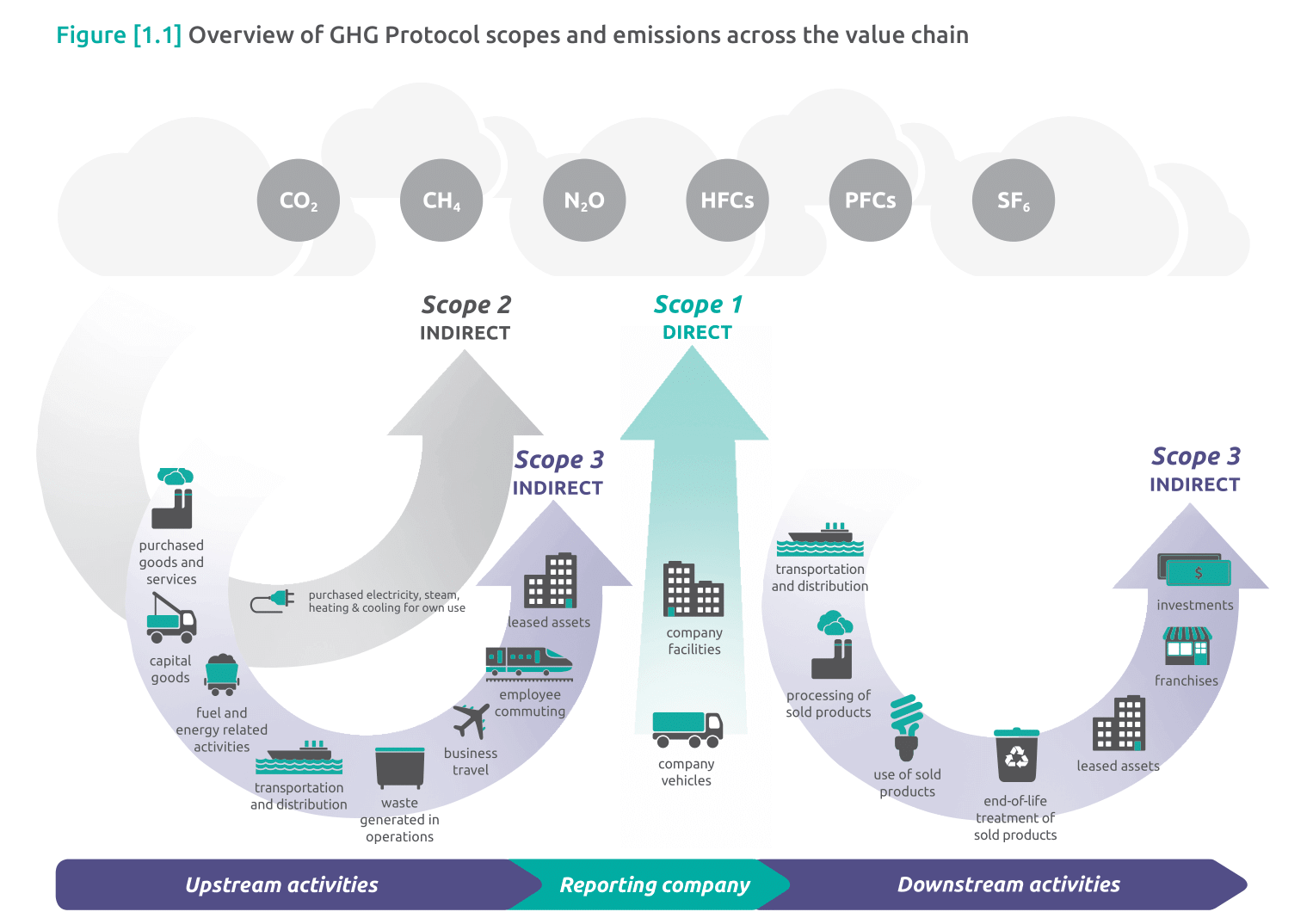

The GHG Protocol established the three scopes of emissions to prevent double counting and provide insights into emissions sources across businesses’ operations and value chains. The GHG Protocol describes each scope as follows:

Scope 1: includes emissions from a company’s owned or controlled operations.

Scope 2: covers indirect emissions from purchased energy consumption.

Scope 3: encompasses all other indirect emissions in the value chain, divided into 15 categories, such as waste disposal, business travel, employee commuting, and product life cycle.

Reducing scope 3 emissions is crucial in the fight against climate change, as these emissions account for, on average, 75% of all companies’ emissions. And in some industries it may ever be higher. However, given that companies have limited direct control over these emissions, collecting data and reducing scope 3 can be extremely challenging, which is why large public companies engage with smaller private suppliers to report and reduce the emissions attributed to them. I think we need to add something here about how the buyers are selecting suppliers who do their best on these issues or are willing to address them.

Although the most pressing requests for ESG data today are related to GHG emissions, a growing number of regulations and companies with ambitious sustainability goals are asking for other sustainability data across their value chain, including diversity, biodiversity, deforestation, plastic waste, board gender diversity, and much more.

Growing Regulatory Landscape and Public Company Ambitions

Countries attempting to provide investors with complete and comparable sustainability information to make informed decisions is driving the creation of new climate and other sustainability disclosure mandates. These mostly apply to publicly traded companies however, in some cases, also to smaller or private companies. The two primary jurisdictions with regulations affecting scope 3 and value chain sustainability are from the SEC in the US and the EU.

The U.S. Securities and Exchange Commission

In March 2022, the SEC released a proposal for Rules to Enhance and Standardize Climate-Related Disclosures for Investors. The proposal would mandate around 4,000 US publicly-traded companies to disclose extensive climate-related information. Importantly the proposals include the disclosure of scope 3 emissions. However, adding scope 3 is one of the main sticking points in finalizing the proposals, so they may or may not be included when the rules are finalized in the second half of 2023.

CSDDD: The CSDDD will affect 4,000 non-EU and 12,800 EU companies. It requires companies to identify, prevent, and mitigate negative human rights and environmental impacts in their operations and value chains. However, companies are not expected to comply with the CSDDD until 2030.

Companies worried about the financial risks of not complying with current and future regulations and with concerns about the other physical and transition risks of ESG risks are taking action to measure their impacts and set ambitious ESG targets.

The number of large publicly-listed companies setting net zero goals, for example, doubled from 2021-23. It is not just climate goals. Companies reporting general sustainability data through the CDP increased by 38% from 2021-22. More companies than ever are measuring and setting targets to reduce their direct and indirect impacts.

The number of larger companies attempting to comply with extensive regulations and setting wide-ranging climate and other ESG goals will inevitably affect the companies across their value chains. Larger companies may begin to include emissions reductions, product material use, and diversity clauses in their supplier contracts.

The growing expectation of smaller private companies to collect, report, and reduce their sustainability impacts could have a huge sway on shaping private companies’ products and strategies.

The Impact on Growing Private Companies

To collect the swathe of data needed to understand the ESG and climate impacts across their supply chains, larger companies are looking to the smaller private companies that supply to them to collect and share the sustainability data attributed to them.

Companies, such as Microsoft, with ambitious supply chain sustainability impact reduction plans, include in their supplier code of conduct that suppliers collect and share emissions for scopes 1, 2, and 3, reduce water consumption, and minimize waste. Microsoft also expects its supplier to provide and achieve plans to reduce absolute GHG emissions by a minimum of 55% by 2030.

Other companies with ESG goals beyond emissions reduction are requiring their suppliers to reduce their own ESG impacts. The outdoor equipment retailer REI has released new product standards that will require their suppliers to eliminate PFAS from the pots, pans, apparel, shoes, bags, packs, and similar gear sold by the retail chain by 2026.

Smaller private companies that fail to collect and share ESG data, with large companies that fall under an ESG disclosure mandate, are a material risk for the larger companies. This could lead to them finding suppliers that can disclose and reduce their ESG impacts.

How Growing Private Companies Can Start Preparing for Scope 3 and Value Chain Sustainability Reporting

Pressure is clearly building on private companies to report on their value chain sustainability impacts, particularly if they are suppliers to larger companies that have set ambitious sustainability targets or need to comply with regulations.

Here are some steps you can take to start preparing for ESG reporting:

1. Understand the Basics of Emissions and Value Chain Sustainability Reporting

The first step is to understand the different scopes of emissions and what value chain sustainability reporting involves. An important thing for smaller private companies to understand is that most large companies will not expect them to measure the emissions and other sustainability factors in their own value chain but only to share the emissions and sustainability factors from their direct operations that can be attributed to the larger companies they supply.

2. Engage with Customers and Other Stakeholders

Engaging with customers and other stakeholders is a key part of managing the expectations of your largest buyers. Helping you understand what sustainability data should be collected and when. This could involve helping customers comply with upcoming regulations and meet targets by collecting and reporting data, working with them to create a joint emissions reduction plan, or reducing other sustainability impacts together.

3. Collect and Report Sustainability Data

Collecting a wide variety of ESG data from many different parts of the company in many different forms may seem daunting. However, creating a hierarchy of importance for data collection, starting with what is most important to your biggest customers, is the best place to start. This will likely be emissions data. Collecting emissions data does not need to be difficult. It can start with spend-based financial data, which can be used for emissions estimates, while more accurate data can be collected as your companies data collection matures matures. Data collection and reporting can be easily achieved through implementing software systems.

Preparing for Scope 3 and value chain sustainability reporting is a significant undertaking, but it can also provide many benefits. It can help companies improve their relationships with and meet the expectations of larger companies and regulators, as well as reduce the ESG-related risks in their own operations.

Good.Lab proved to be the right partner to support Protingent in producing an accurate GHG emissions baseline across Scopes 1, 2, and 3, calculating their service level emissions, and providing guidance in setting targets for emissions reduction to comply with Microsoft’s requirements.

Good.Lab has been instrumental in guiding Protingent through complying with Microsoft’s supplier code of conduct, particularly in meeting the complex emissions reporting requirement.

The number of companies expecting their suppliers and other stakeholders in their value chain to share sustainability information is growing daily. The inclusion of scope 3 and other value chain sustainability factors in upcoming regulations will supercharge these requests.

Measuring emissions and sustainability impacts to help larger publicly traded companies measure and mitigate their scope 3 and value chain sustainability is an opportunity for growth, reputation enhancement, and long-term resilience that growing private companies cannot miss.

Disclaimer: Good.Lab does not provide tax, legal, or accounting advice through this website. Our goal is to provide timely, research-informed material prepared by subject-matter experts and is for informational purposes only. All external references are linked directly in the text to trusted third-party sources.

Gary Gao, CEM, PMP, SEA

Senior Manager

Gary has over 10 years of experience in the energy and sustainability space. He excels in developing holistic energy and sustainability strategy, engaging stakeholders and guiding clients through their sustainability journey. His breadth of experience is diverse and expansive from working with many Fortune 500 clients to being educated in multidisciplinary fields of engineering, environmental policies, and business.

Ready to elevate your sustainability efforts?

Connect with our sustainability experts today!

From sustainability program development to target setting, data management, and reporting, our team can help you fast-track building a world-class sustainability program.

CDP Reporting for Manufacturers: What to Do When a Customer Asks

The CDP portal opened on April 27th. If you received a customer request to disclose and you’re not sure what to do with it, here’s what you need to know. In 2025, of the 23,100+ companies who reported through CDP’s Supply Chain program, more than a third were manufacturers. And more than half of those […]

Customer Asked for Your EcoVadis Score? Here’s What That Means for Your Manufacturing Business

Perhaps the email asking for your EcoVadis score came from your customer’s procurement team, or you found it buried in a supplier onboarding form. Either way, it’s sitting in your inbox, and you’re not sure what to do with it. If you’re wondering what receiving an EcoVadis request as a manufacturer means for your business, […]

State Climate Reporting Laws: A Guide to US Climate Disclosure Laws

Federal climate disclosure rules may be stalled, but state climate reporting laws are not – and for large companies operating across the US, the compliance clock is already running. The situation is more manageable than it looks. Most state rules are built from the same blueprint: California moved first, and every state that followed used […]

Welcome to Good.Lab! We're glad you're here and want you to know that we respect your privacy and your right to control how we collect and use your personal data. Please read our Privacy Policy to learn about our privacy practices or to exercise control over your data.