The Corporate Sustainability Reporting Directive (CSRD) is a directive by the European Union designed to make sustainability and ESG (environmental, social, governance) reporting by companies more comprehensive, consistent, and aligned with financial reporting standards.

The CSRD is currently the most comprehensive sustainability reporting regulation globally. Achieving compliance will demand comprehensive and accurate reporting by certain companies on more than 1,100 sustainability metrics beginning in 2025.

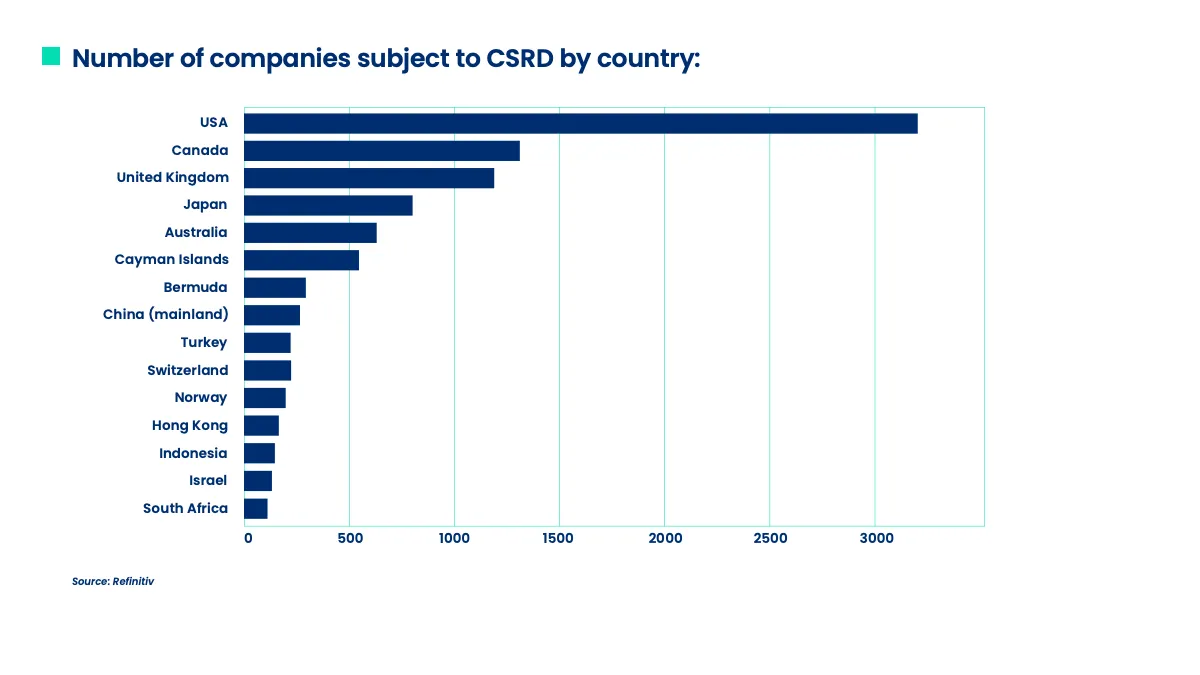

The CSRD may have its roots in the European Union, but its impact is expected to reach far beyond its borders. The CSRD will affect over 10,000 non-EU companies, including 3,000 from the U.S., along with an estimated 50,000 EU companies.

Time is crucial for U.S. companies to gear up for this extensive regulation. The CSRD significantly expands the scope of required reporting beyond current U.S. mandates, such as those set forth by the SEC and California, which focus exclusively on climate.

Key Takeaways:

- The CSRD will have the widest impact of any global sustainability regulation, affecting 50,000 EU and 10,000 non-EU companies (3,000 of which are U.S. companies).

- The CSRD will require impacted companies to disclose a comprehensive list of sustainability data annually, based on a double materiality assessment, using the EU’s Sustainability Reporting Standards (ESRS).

- Now is the time to start preparing for this new comprehensive and pervasive sustainability disclosure. Businesses will need to scale up quickly on new skills, tools, and processes to ensure CSRD compliance.

What is the EU Corporate Sustainability Reporting Directive (CSRD)?

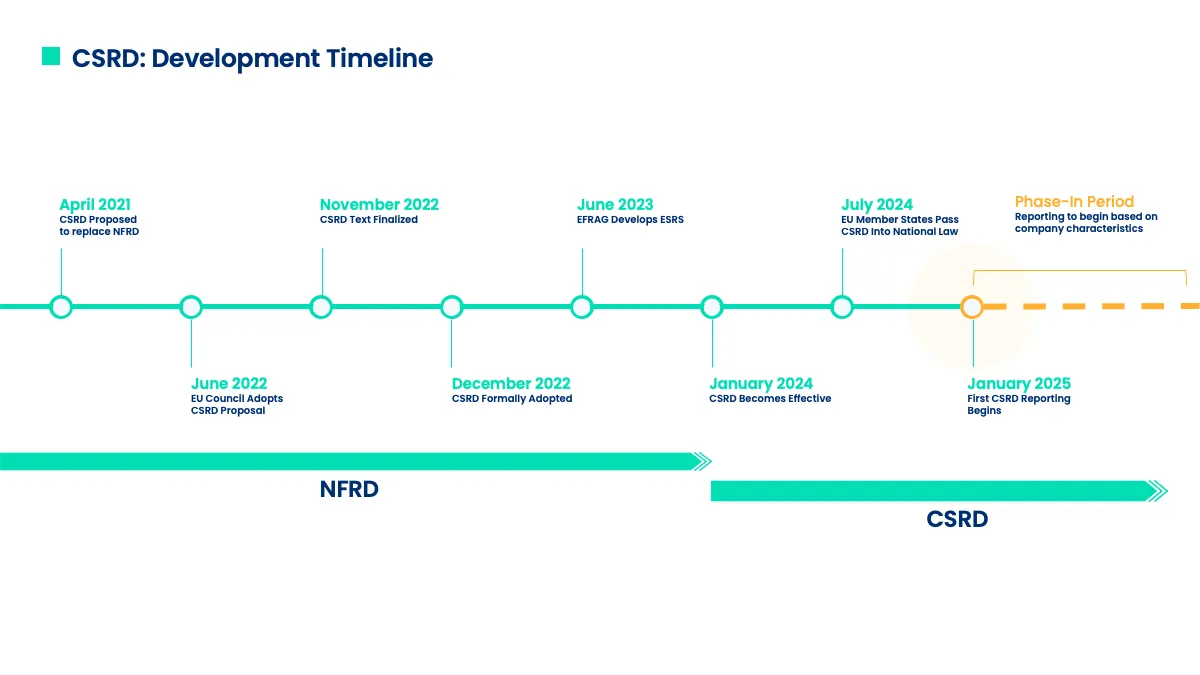

The EU Commission established its European Green Deal in 2019 to transform the region into a modern, resource-efficient, and competitive economy. In 2021, it announced the adoption of the EU Corporate Sustainability Reporting Directive (CSRD) in line with the commitments made under the EU Green Deal.

The CSRD was formally approved in January 2023 and will replace the EU’s previous reporting regulation, the Non-Financial Reporting Directive (NFRD), in 2024.

The CSRD significantly expands the scope of companies required to report and the sustainability information that needs to be disclosed, promoting transparency and accountability in corporate sustainability practices.

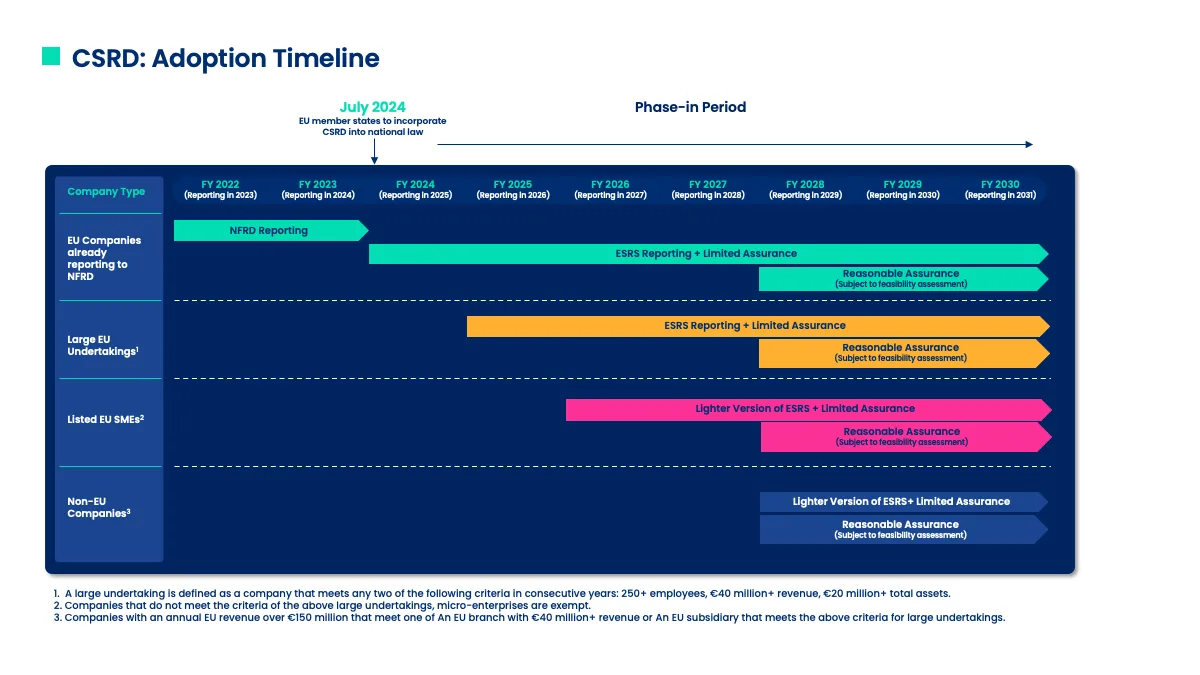

To comply with the CSRD, covered companies must start making annual sustainability reports in 2025, with a phased-in implementation based on specific company characteristics.

Companies must use the European Sustainability Reporting Standards (ESRS) for CSRD disclosure, which were developed by the EU’s standard-setting body, the European Financial Reporting Advisory Group (EFRAG) which must be put into Member States national law by July 2024. All CSRD disclosures are subject to third-party audit assurances.

Key Features:

- Expanded Scope: CSRD significantly expands the number of companies required to report on sustainability (from 11,000 under the NFRD to over 50,000 EU companies). It also affects non-EU companies (~10,000) that operate within the EU or meet certain thresholds.

- Double Materiality: Companies must report on both the impact of their activities on the environment and society (outward impact) and how sustainability issues affect the business (inward impact).

- Reporting Standards: The CSRD mandates companies to follow the European Sustainability Reporting Standards (ESRS), which provide detailed guidelines on the more than 1,100 sustainability metrics that need to be disclosed.

- Third-Party Assurance: Companies are required to have their sustainability reports audited or assured by an independent third party. Beginning with limited assurance but moving to more in-depth reasonable assurance in 2028 (subject to a feasibility assessment). Check out our guide to audit readiness to ensure you are prepared.

- Phased-In Implementation: The requirements will be phased in over several years, starting with large public-interest entities before expanding to other companies.

Who needs to comply with the EU Corporate Sustainability Reporting Directive (CSRD)?

The CSRD has the largest scope of any global sustainability reporting regulation. It requires 50,000 EU and 10,000 non-EU companies to report annually. Determining if your company must comply with the CSRD and the timing of reporting can be challenging.

Here is an overview of the characteristics of companies that are subject to the CSRD:

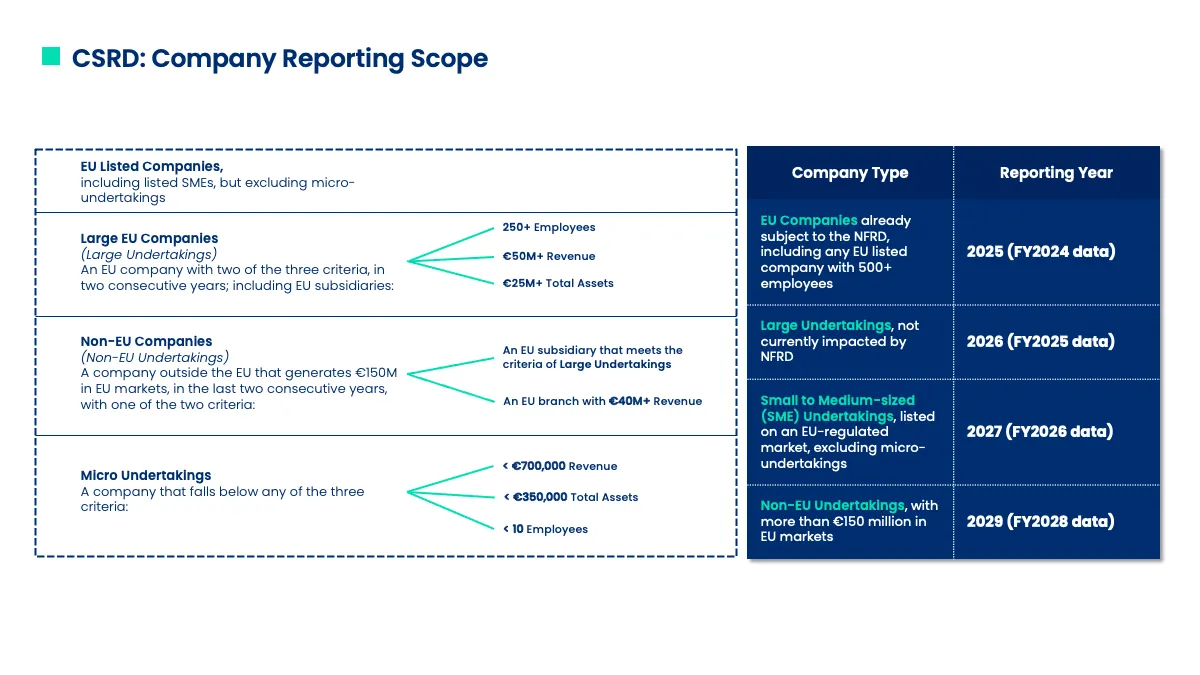

CSRD for European Companies

While the NFRD covered only 11,600 listed EU companies and banks, based on headcount, revenue, and asset balance criteria, the expanded scope of the CSRD will require an additional 39,000 EU companies to disclose sustainability metrics.

Here are the characteristics of EU companies that are subject to the CSRD:

- EU Companies already subject to the NFRD, to begin reporting in 2025 based on data from FY2024.

- EU Large and Listed Companies (Large Undertakings) will begin reporting in 2026 based on data from FY2025. A large undertaking is defined as a company that meets any two of the three following characteristics in consecutive years:

- Over 250 employees

- Net revenue over €50 million

- Total assets over €25 million

- EU Listed Small to Medium-sized Enterprises (SME), that do not meet the criteria of the above large undertakings, to begin reporting in 2027 based on data from FY2026, however, in some cases, that can be delayed a year.

- EU Micro-enterprises are exempt, which the regulation defines as meeting any one of the three following characteristics:

- Under ten employees

- Net revenue under €700,000

- Total assets under €350,000

CSRD for U.S. Companies

The adoption timeline for the CSRD is short compared to U.S. climate reporting regulations, like the SEC Climate Disclosure rule and California’s SB 253 & 261. Some U.S. companies with certain characteristics will need to begin CSRD reporting as early as 2026.

Here are the characteristics of U.S. companies that are subject to the CSRD:

- U.S. Companies with Large EU Subsidiaries (a subsidiary is a separate legal entity from its parent company), to begin reporting the sustainability metrics of the subsidiary in 2026 based on data from FY2025; in 2029, they are to broaden reporting to cover the entire global company, if they meet any two of the three following criteria in consecutive years:

- Over 250 employees

- Net revenue over €50 million

- Total assets over €25 million

- U.S. Companies with net revenue over €150 million in EU Markets, to begin reporting on data covering the entire global parent company in 2029 based on data from FY2028, using a lighter version of the ESRS, if they meet any one of the two following criteria:

- An EU branch, (a branch is an extension of a company, but under the same legal entity), with over €40 million in net revenue

- An EU subsidiary that meets the above criteria for large undertakings, e.g., any two of the following three criteria:

- Over 250 employees

- Net revenue over €50 million

- Total assets over €25 million

The parameters by which U.S. companies report are also the same for the other 7,000 companies across the world that meet the criteria for CSRD applicability.

Companies Indirectly Affected by CSRD

Although the CSRD directly affects about 60,000 companies, the nature of its disclosure requirements has broader global implications as it mandates companies to report on value chain sustainability data, including Scope 3 emissions.

👉 The companies subject to the CSRD will be seeking more sustainability data from their supply chain partners and collaborating with other stakeholders to collect and share relevant information.

When do companies need to comply with the EU Corporate Sustainability Reporting Directive (CSRD)?

The CSRD has been approved by the European Commission and is now being implemented into law. Compliance will be phased in based on company size and other specific characteristics.

The following timeline provides an overview of which companies must report to CSRD and when, categorized by their size and jurisdiction:

- 2025: EU companies already reporting to NFRD will start reporting on FY2024 data.

- 2026: Large undertakings will start reporting on FY2025 data.

- 2027: Listed EU SMEs will start reporting on FY2026 data, using a lighter version of the ESRS.

- 2029: Non-EU companies with €150m net revenue in the EU in both of each of the last 2 years will start reporting on FY2028 data, using a lighter version of the ESRS.

All companies in the CSRD’s scope are required to obtain limited assurance from a third-party verifier in their first reporting year. The need to obtain reasonable assurance is scheduled for 2028, subject to a feasibility assessment.

What do companies need to disclose to the EU Corporate Sustainability Reporting Directive (CSRD)?

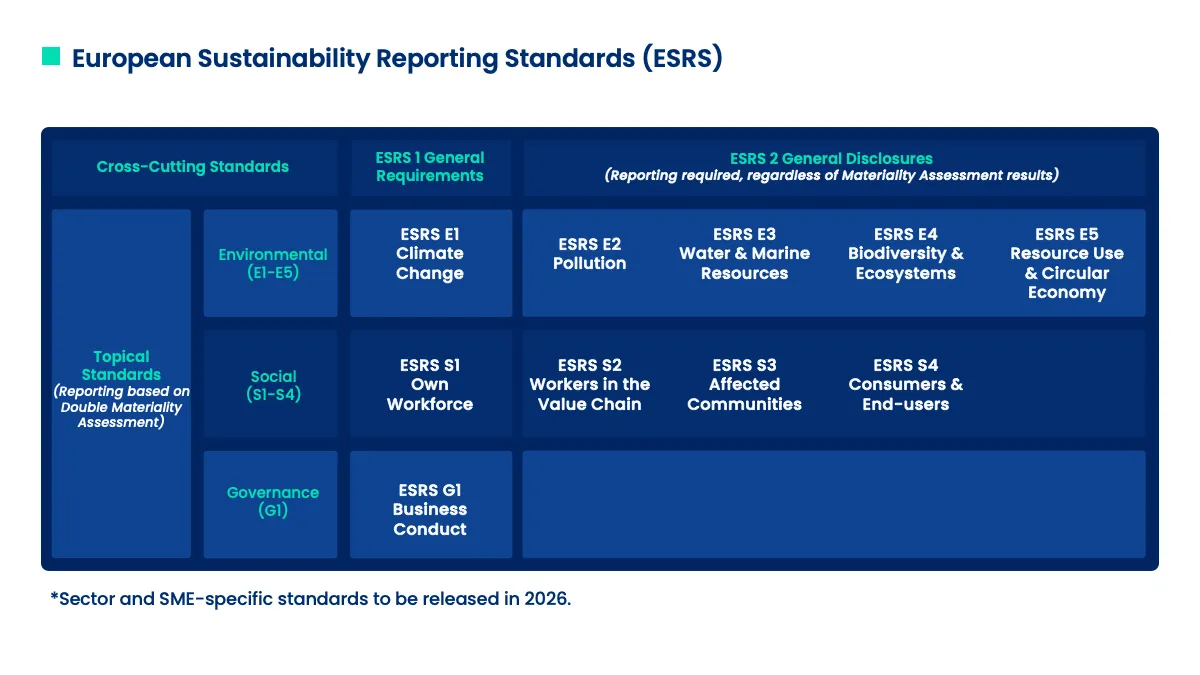

The CSRD mandates that companies submit an annual sustainability report alongside their financial reporting to their member state. Reporting must comply with the technical standards set forth in ESRS, a set of EU compliance and disclosure requirements developed by EFRAG. ESRS are organized into two foundational standards, ESRS 1 and ESRS 2.

ESRS 1 General Requirements are the principles that companies must follow to comply with the CSRD. ESRS 1 helps companies understand and define what needs to be reported annually and introduces them to concepts, such as double materiality, determining value chain boundaries, when to report, and how information should be presented. ESRS 1 includes information about the following:

- Categories of standards and disclosures

- Qualitative characteristics of information

- Double materiality as the basis for sustainability disclosures

- How to conduct sustainability due diligence

- Value chain definitions and boundaries

- Time horizons for disclosure

- How to prepare and present sustainability information for compliance

ESRS 2 General Disclosures define what companies must report on to comply with the CSRD. ESRS 2 is split into four sections that cover general and topical sustainability disclosures:

1. General Disclosures

Companies are required to make general disclosures, whether they are material or not, in order to produce a comprehensive portrait of a company's sustainability approach and how it aligns with broader ESG objectives.

👉 ESRS 2 disclosures closely align with the Taskforce on Climate-Related Financial Disclosures (TCFD) reporting framework. Companies that align their sustainability reporting with TCFD are already ahead of the curve for CSRD compliance and other reporting mandates.

As part of the general disclosures, companies are expected to report on governance, strategy, impact assessment, risk management, and other core aspects of sustainability performance, plus, the company's due diligence policies, how they engage with stakeholders for data, and how the company conducted their double materiality assessment to determine which topical disclosures they must disclose.

CSRD Topical Disclosures

Companies must determine which of the ten topical disclosure standards across ESG criteria are material to their business by conducting a double materiality assessment. For each topic deemed to be material, companies must collect data and disclose all relevant data points within those standards.

2. Environmental Disclosures

- ESRS E1 Climate Change

- This will be material for most companies and requires disclosure of Scope 1, 2, and 3 GHG emissions, climate risks, energy use, and climate transition plans. Emissions measurements are based on the guidance in the Greenhouse Gas Protocol.

- Example question: Expected GHG emission reductions (tC02e)

- ESRS E2 Pollution

- Includes disclosure of any air, water, and land pollution, both in the company’s operations and value chain.

- Example question: Microplastics generated (mass)

- ESRS E3 Water and Marine Resources

- Includes disclosure of any water use, recycling, and any impacts on marine environments, in its operations or value chain.

- Example question: Total water consumption (volume)

- ESRS E4 Biodiversity and Ecosystems

- Includes the disclosure of material impacts on natural environments and any biodiversity loss mitigation strategies, in the company’s operations and value chain.

- Example question: Scope of resilience analysis along own operations and related upstream and downstream value chain (narrative)

- ESRS E5 Resource Use and Circular Economy

- Includes disclosure of material waste types, quantities, and circularity resource mapping across the company’s operations and value chain.

- Example question: Rates of recyclable content in products (percent)

3. Social Disclosures

- ESRS S1 Own Workforce

- Includes disclosure of material information on gender and diversity numbers, and information on labor and human rights policies.

- Example question: Policies explicitly addressing trafficking in human beings, forced labor or compulsory labor and child labor (semi-narrative)

- ESRS S2 Workers in the Value Chain

- Includes disclosure of material information on value chain employment policies on slave labor, human trafficking, and value chain working conditions.

- Example question: Description of relevant human rights policy commitments relevant to value chain workers (narrative)

- ESRS S3 Affected Communities

- Includes disclosure of material information on the company’s impact on the communities they operate in.

- Example question: Disclosure of how perspectives of affected communities inform decisions or activities aimed at managing actual and potential impacts (narrative)

- ESRS S4 Consumers and End-users

- Includes disclosure of material information on the company’s impact on end users of products and services.

- Example question: Disclosure of general approach in relation to respect for human rights of consumers and end-users (narrative)

4. Governance

- ESRS G1 Business Conduct

- Includes disclosure of the company’s material governance information, such as the cash amount spent on lobbying, executives' pay tied to sustainability performance, company procedures for corruption, bribery, and transparency.

- Example question: Description of approaches regarding relationships with suppliers, taking account risks related to supply chain and impacts on sustainability matters (narrative)

EFRAG is currently working on additional standards for sector-specific reporting and for non-EU companies. These are scheduled to be released in June 2026.

CSRD reporting must be submitted in a compliant electronic reporting format, e.g., a digital, machine-readable XBRL (XHTML) format to facilitate data analysis, sharing, and comparison. Submissions are to be made within 12 months of a company's fiscal year end.

CSRD reporting also requires limited data assurance in the first years of reporting, and in some instances depending on feasibility, reasonable data assurance will be required beginning in 2028 from a third-party auditor, such as the independent CPA firms in Good.Lab's partnership network.

CSRD & Double Materiality

Unlike most existing sustainability reporting frameworks, the CSRD notably adopts a double materiality framework, which evaluates two dimensions of materiality, both the financial effects of environmental, social, and governance issues on the company and the company’s impact on the climate, environment, and society.

Single Materiality considers how climate and other ESG risks and opportunities impact a company’s financial performance, operations, physical assets, and position.

Most single materiality reporting frameworks focus only on financial materiality, however, GRI is the exception that considers a company’s impact on the climate, environment, and society.

Double Materiality considers both the impact a company has on the climate, environment, and society and the effect of climate and other ESG risks and opportunities on its financial performance.

The two dimensions of Double Materiality for the purposes of CSRD reporting are:

- Impact Materiality: Looks at how a company impacts the climate, environment, and society.

- Financial Materiality: Looks at how climate and other ESG risks and opportunities affect a company’s finances.

A disclosure topic is considered to be material if it aligns with either dimension of materiality or both. It must be reported to CSRD if deemed material by either dimension.

To identify significant impacts, risks, and opportunities, companies are required to conduct a double materiality assessment prior to CSRD reporting. Additionally, companies must document and report the process used for determining materiality, ensuring transparency and accountability in their assessments.

How to comply with the EU Corporate Sustainability Reporting Directive (CSRD)?

CSRD will transform sustainability reporting for companies, as it introduces a heightened level of complexity. Most companies will need to scale up their capabilities around ESG metric measurement and reporting to comply.

It will also apply to smaller companies, requiring them to establish new processes to ensure transparency and meet the new requirements, including double materiality assessment.

Here are actions your company can take now to prepare for CSRD reporting:

- Understand CSRD Requirements and Timeline: Determine your company's reporting obligations based on size and jurisdiction. Identify the applicable ESRS standards that apply to you, including sector-specific disclosures when available, and assess whether your company qualifies for a lighter reporting obligation.

- Conduct a Double Materiality Assessment: Perform a double materiality assessment to identify relevant impacts, risks, and opportunities that align with the CSRD framework. Ensure the assessment process itself is properly documented for disclosure.

- Analyze Current Gaps and Build a Cross-Functional Team: Conduct a gap analysis comparing your current sustainability reporting practices against CSRD standards. Identify any ESG data collection gaps and build a team to manage compliance, data accuracy, and integration into financial reporting.

- Implement Data Management and Reporting Processes: Invest in sustainability data management tools, like Good.Lab's sustainability software, that can help you collect, calculate, and collate relevant ESG metrics. An external expert specializing in sustainability reporting and compliance can guide your materiality assessments and help you develop CSRD compliant reporting processes.

- Plan for Assurance: Implement quality control measures, prepare for, and obtain third-party assurance for your data. You may also consider training internal staff and stakeholders on CSRD requirements and consider how you will stay up to date with other evolving regulations.

CSRD Reporting with Good.Lab

CSRD compliance requires meticulous preparation. To comply with the CSRD, companies must not only conduct a double materiality assessment but also obtain independent assurance for their sustainability reports.

To prepare for CSRD reporting, companies new to sustainability reporting will need to define processes for collecting sustainability-related data and companies with prior experience should reflect on past learnings and look for opportunities to consolidate collected information.

By establishing a solid foundation and developing robust governance protocols now, companies will be better equipped to meet future sustainability reporting requirements.

At Good.Lab, we engage with businesses daily to help them navigate this evolving landscape and transform sustainability challenges into strategic opportunities.

Here is how we help companies meet the reporting requirements of CSRD:

- Determine company applicability for CSRD reporting

- Hands-on guidance, and access to an experienced ESG expert

- Development of an overarching sustainability strategy and action plan

- Software tools to quickly conduct a Double Materiality Assessment

- Collection, calculation, and preparation of emissions, climate, and other ESG metrics

- A CSRD-compliant sustainability report in XBLR form

What is CSRD? The Corporate Sustainability Reporting Directive (CSRD) is an EU directive that expands companies' sustainability reporting requirements from their previous reporting framework, the Non-Financial Reporting Directive (NFRD). It aims to provide greater transparency on environmental, social, and governance (ESG) issues, enhance accountability, and help the EU meet its Green Deal.

What is ESRS? The European Sustainability Reporting Standards (ESRS) are a set of standards the EU developed, which companies need to use to comply with the CSRD. These standards ensure that reports are comparable, reliable, and relevant for users.

What is EFRAG (European Financial Reporting Action Group)? The European Financial Reporting Action Group (EFRAG) is the group the EU created to create reporting standards, frameworks, and regulations. EFRAG created the CSRD and ESRSs.

Who needs to report to CSRD? Under the CSRD, the reporting requirements will apply to all large companies, whether they are publicly listed or not, that meet two out of three criteria: having more than 250 employees, a net revenue of more than €50 million, or a balance sheet total of more than €25 million. Additionally, all companies listed on regulated markets (except micro-enterprises) are required to comply, regardless of size. The directive will also gradually apply to non-EU companies with significant activity in the EU market, specifically those with a net revenue of more than €150 million in the EU.

What needs to be reported to CSRD? Companies must report on a wide range of ESG metrics under the CSRD. Companies need to report against a data set of more than 1,100, which includes things like the companies’ impact on the environment, climate, social matters, treatment of employees, respect for human rights, anti-corruption and bribery issues, and board diversity. Reporting is based on a double materiality assessment.

How to report to CSRD? Companies should compile their annual sustainability reports in line with the needs of CSRD within their typical financial reporting. To simplify the process, reporting data must be in a machine-readable digital XBLR form.

How does the CSRD compare to the SEC Climate Disclosure rule? The CSRD and the SEC's climate-related disclosures both focus on providing transparency on sustainability issues. However, the CSRD is broader in scope, covering a wide range of ESG metrics, whereas the SEC rules are specifically targeted at climate-related disclosures.

How does the CSRD compare to the California Climate Rule? The CSRD is more comprehensive than the California climate rules, which are more specifically targeted at emissions and climate-related risks for U.S. companies operating in California. The CSRD includes detailed reporting on a broader set of sustainability metrics, applying to a wider range of companies across the EU and globally.

How does the CSRD compare to the ISSB (International Sustainability Standards Board)? The International Sustainability Standards Board (ISSB) standards and the CSRD standards are both comprehensive sustainability disclosure frameworks. However, the CSRD is mandatory, and the ISSB is voluntary. Plus, the CSRD is based on double materiality, and the ISSB is based on single materiality. Despite their differences, the two reporting frameworks work closely together to ensure interoperability. They also released an interoperability guide to help reporters align their data with both concurrently.

FAQs

The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation requiring certain companies to disclose detailed information on their environmental, social, and governance (ESG) impacts. It helps businesses improve transparency, build trust with stakeholders, and align with sustainable practices, while ensuring compliance with EU laws.

CSRD applies to large EU companies, certain non-EU companies with significant EU operations, and listed SMEs. If your company meets the size or turnover thresholds, you’ll need to comply. Even if not directly in scope, many businesses are indirectly affected through supply chain requirements.

Good Lab provides expert guidance, streamlined data collection, and robust ESG reporting frameworks to help you meet CSRD requirements efficiently. We ensure your disclosures align with European Sustainability Reporting Standards (ESRS) and are audit-ready.

Businesses must report on a wide range of sustainability metrics, including climate change impacts, energy use, diversity, human rights, supply chain practices, and more. Reports must follow the ESRS framework and cover both risks and opportunities.

CSRD implementation is phased, starting in 2024 for the largest companies, with other categories following in subsequent years. Acting early helps businesses prepare, reduce compliance risk, and position themselves as sustainability leaders.