After a two-year wait, the U.S. Securities and Exchange Commission (SEC) has officially passed a groundbreaking climate disclosure rule that sets a clear course for business sustainability efforts and provides decision-useful climate risk disclosures to investors. The finalized rule was voted through 3-2 on Wednesday, March 6th, 2024 and will require companies listed on the U.S. stock market to report climate-related risks beginning as early as 2025.

After receiving an unprecedented 24,000 comment letters, the finalized rule was scaled back from the initial proposals set forth in March 2022, however, the finalized climate rule still marks a significant milestone for U.S. companies around sharing consistent, comparable, and reliable climate-related data.

By the end of this post, you will have a better understanding of the specifications of the SEC's climate disclosure rules, the types of companies that need to report, and the timeline for reporting. You will also learn how the finalized climate rule will impact the wider economy and private companies, the challenges of disclosure, and best practices on how to prepare for compliance.

Key Takeaways from the SEC Climate Rule

With so much commentary surrounding the bill and an 886-page document to sift through, for a TL;DR, here are four main takeaways from the final SEC climate rule that you need to know now:

- Scope 1 and 2 Greenhouse Emissions: Large Accelerated Filers (LAF) and Accelerated Filers (AF) are expected to report on and obtain assurance for material Scope 1 and 2 emissions. Smaller companies are exempt. All companies are exempt from disclosing Scope 3.

- Material Climate Risks: All covered reporters will be expected to share financially material climate risks in accordance with the guidelines of the Taskforce on Climate-related Financial Disclosures (TCFD), including material climate risks, and the process used for identifying, assessing, and mitigating them, their impacts on company finances, and their governance.

- Phase-in Period: The final rules extend disclosure timelines and will be phased in over the next ten years. Smaller companies are not expected to begin disclosing climate risks until 2028, and assurances will begin in 2030.

- Attestation: Third-party auditing for emissions assurances will be required for LAF and AF, starting with limited assurance in 2030 and 2032, respectively. Only LAF will be required to acquire reasonable assurance on emissions beginning in 2034.

What is the SEC Climate Rule?

The SEC's final climate rule, also known as, The Enhancement and Standardization of Climate-Related Disclosures for Investors is the first federal climate reporting regulation in the U.S.

The rule was originally proposed in March 2022 as a means to provide investors with decision-useful, consistent, and comparable climate-related risk and emissions data in order for them to make more informed investment decisions.

Two years later, the SEC voted through a final version of the rule, which, although scaled back from the original, is still a huge step toward all U.S. companies sharing and tracking their emissions data and climate risks in a standardized manner.

The SEC's accompanying Fact Sheet is a helpful tool for understanding what your company may need to disclose without needing to read U.S. SEC, August 12, 1999.

What is included in the SEC Climate Rule?

The final SEC climate-related disclosure rule requires public companies to provide certain climate-related financial data and greenhouse gas emissions insights in public disclosure filings.

Here is a run-down of the climate-related information that registrants must share when deemed material:

Greenhouse Gas Emissions

- Carbon accounting and reporting on Scope 1 and 2 greenhouse gas (GHG) emissions is required for LA & AF, when deemed material. Smaller companies are exempt from Scope 1 and 2 reporting.

- LAF and AF are expected to obtain limited assurance on Scope 1 and 2 emissions reporting, and LAF are expected to obtain reasonable assurance on their emissions reporting.

- The SEC has provided accommodations for companies to report their GHG emissions in 10-Qs (or 20-Fs for foreign filers), as opposed to 10-Ks for all other reporting. The timeline extends to the second quarter of the reporting year in order to give more time to collect data and reduce the burden of climate reporting.

Climate-related Risk

All registrants will have to disclose material climate risks, climate-related material expenditures, and impacts on financial estimates. Here is a breakdown of the climate-related risk reporting that is required:

- TCFD-aligned Climate Risk Reporting: Climate risk reporting for the SEC final rule is largely in line with the guidelines of the Taskforce on Climate-Related Financial Disclosures (TCFD) and include:

- Any climate risks that are reasonably likely to have a material impact on the registrant’s business strategy, results of operations, or financial condition over the short, medium, and long term

- The potential and actual material impacts of these climate risks

- A quantitative and qualitative description of the costs of building a strategy to mitigate and assess material climate risks

- Any governance structure that is implemented for managing material climate risks

- Any transition plans, scenario analysis, or internal carbon prices used to mitigate or adapt to material climate risks.

- Climate Goals and Targets: Companies have to share any climate goal or target that has been set and is material to a reporting companies' finances.

- Carbon Offsets: The capitalized costs, expenditures expensed, and all other financial implications related to carbon offsets that are material to climate goals and targets.

- Physical Climate Risks: The costs, expenditures, and charges incurred as a result of physical climate risks, such as severe weather events and sea level rise. This is the only non-material issue and should be reported when the physical climate risk represents a threshold of greater than a 1% of turnover before tax.

How does the SEC view materiality?

The SEC adheres the Supreme Court definition of materiality that a fact is material if there is:

a substantial likelihood that the . . . fact would have been viewed by the reasonable investor as having significantly altered the "total mix" of information made available.

Because materiality is central to almost all disclosures under the SEC’s final climate rule, companies are advised to conduct a materiality assessment well in advance of collating climate data in order to evaluate the material nature of their climate-related risks, carbon emissions, and costs to determine their reporting requirements for future disclosure.

How are companies affected by the SEC Climate Rule?

Most public companies that are on the U.S. stock exchange will be impacted by this new rule, as will some private companies. The extent to which each type of listed company is impacted depends on its reporting status and size.

Here is a breakdown of each registration category and the specific climate risks and emissions data they are expected to disclose:

- Large Accelerated Filers (LAF): Issuers with a public float of > $700M (~2,500 companies): LAF will be expected to report the soonest, with their first reporting of climate risks beginning in 2026 for FY25. They will also be expected to share their Scope 1 and 2 GHG emissions in 2027 for FY26 and obtain limited assurance on emission data three years later and reasonable assurance seven years later.

- Accelerated Filers (AF): Issuers with a public float between $250-700M (~900 companies): AF will be expected to share their first climate risk report beginning in 2027 for FY26. They also have to share their Scope 1 and 2 GHG emissions in 2029 for FY28 and obtain limited assurance on emission data three years later.

- Non-Accelerated Filers (NAF): Issuers with a public float < $75M or that have a public float of $75M+ and < $100M in revenues: NAF will be expected to report on their material climate risks in 2028 on FY27 data and on climate-related material expenditures and impacts on financial estimates in the following year.

- Smaller Reporting Company (SRC): Issuers with a public float of $75-250M and annual revenues under $100M: Same coverage as NAF.

- Emerging Growth Companies (EGC): Recent IPO companies with annual revenue under $1.235: Same coverage as SRC and NAF.

Which companies need to report on what, and by when?

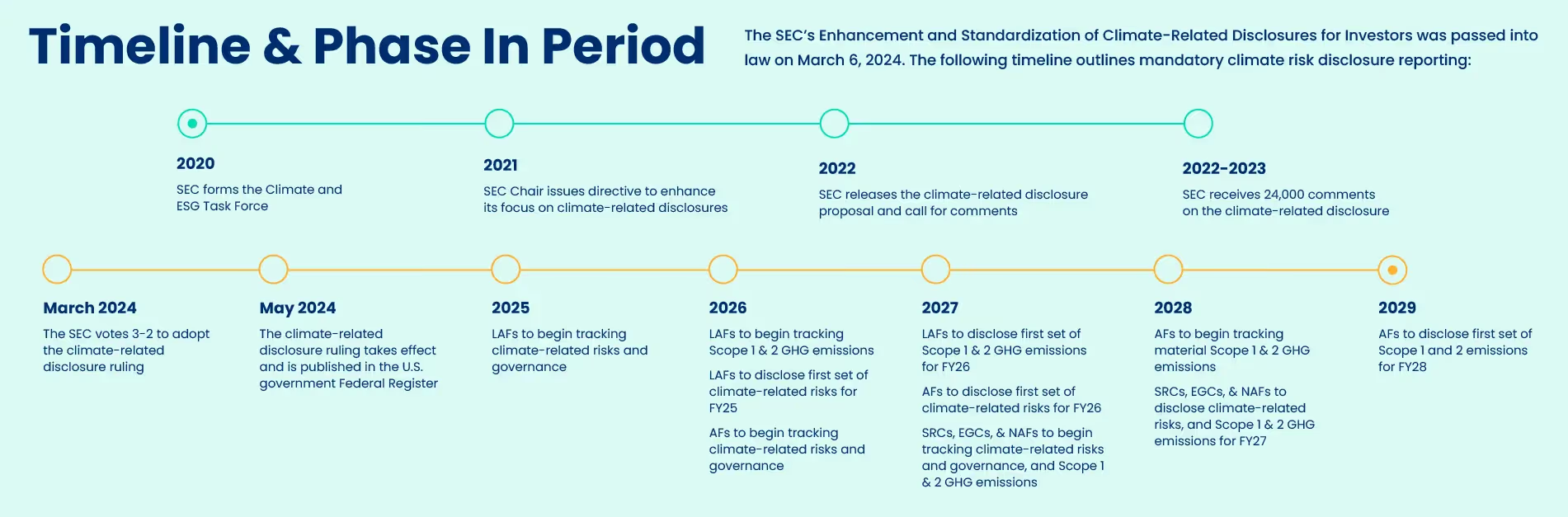

The reporting timeline for the SEC climate rule will be phased in over the next ten years. The reporting requirements will begin soonest for the largest companies before smaller companies are slowly brought into the reporting fold.

Here is a brief overview of the SEC’s regulatory timeline:

- March 6, 2024: The final rule for The Enhancement and Standardization of Climate-Related Disclosures for Investors is approved by a 3-2 vote.

- 2025: The largest companies under the rule, LAFs, will begin collecting climate risk and governance data for their first report in 2026.

- 2026: AF will begin collecting climate risk and governance data for their first report in 2027. LAFs will make their first climate-related risk disclosure in their SEC filings and begin to collect material Scope 1 and 2 emissions data.

- 2027: AFs will make their first climate-related risk disclosure in their SEC filings. LAFs will make their first report containing material Scope 1 and 2 GHG emissions data. NAFs, SRCs, and EGCs will begin collecting climate risk and governance data for their first report in 2028.

- 2028: NAFs, SRCs, and EGCs will make their first climate-related risk disclosure in their SEC filings on FY27 data. AFs begin to collect material Scope 1 and 2 emissions data

- 2029: AFs will make their first report containing material, Scope 1 and 2 GHG emissions data.

- 2030: LAFs will need to have their material, Scope 1 and 2 GHG emissions data assured using limited assurance.

- 2032: AFs will need to have their material, Scope 1 and 2 GHG emissions data assured using limited assurance.

- 2034: LAFs will need to have their material, Scope 1 and 2 GHG emissions data assured using reasonable assurance.

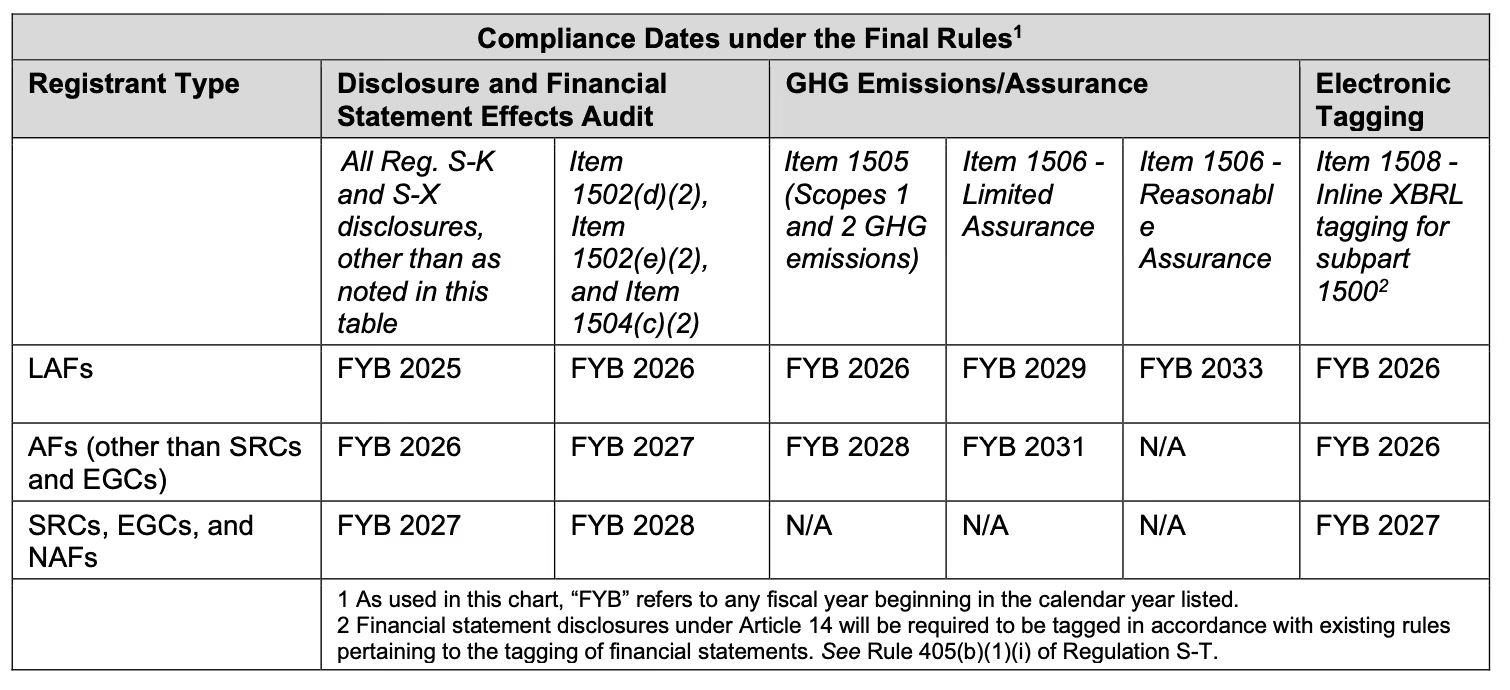

Table 1. Timetable for SEC Climate Rule Disclosure

The final rules will become effective 60 days after publication in the Federal Register, and compliance will be phased in as follows:

What are the attestation requirement for the SEC Climate Rule?

Mandatory Assurance

The final SEC climate rule will require LAFs and AFs to obtain limited assurance on their Scope 1 and 2 GHG emissions three years after their first filing (2029 and 2031, respectively), and LAFs will have to obtain reasonable assurance for their emissions reporting beginning seven years after their first filing (2033).

Voluntary Attestation

The SEC also stipulates that any filer that voluntarily obtains attestation must share information, such as who conducted the assurance, what standard was used, a brief description of the results of the assurance, the type of assurance (reasonable or limited), and if the assurance provider has any conflicts of interest with the filer. The SEC therefore anticipates that attestation services may extend far beyond just those companies that are impacted by mandatory attestation.

Penalties for Non-Compliance

The SEC does not specify penalties for non-disclosure, however, the rule states that any penalties will be subject to the severity of the non-compliance and whether the non-disclosure was intentional or not. It is important to note that in recent years, the SEC has issued millions of dollars in fines for greenwashing and misstatement of environmental goals and achievements. The largest of such fines so far was in 2023, when Deutsche Bank was fined $19 million for misstating (greenwashing) the ESG performance of their funds. Non-compliance also carries substantial reputational risks, which 55% of companies now consider a top 5 operating risk.

How will the SEC Climate Rule affect private companies?

Although private companies are not bound directly by SEC reporting rules, the trend towards enhanced climate reporting will still affect them. Managing climate related risks is becoming a best practice, and between California, EU, and SEC climate rules, the vast majority of enterprise companies will need to develop or enhance a climate risk and reporting strategy.

Here are five ways that private and early-growth stage companies will be impacted by the SEC climate rule:

- Climate Risk Information Requests: Given that the rule still requires companies to assess material value chain climate-related risks impact the registrant’s business, results of operations, or financial condition, it is expected that supply chain climate data request pressures will continue to accelerate as companies request climate information from smaller companies in their supply chain.

- Increased Stakeholder Expectations: The emphasis on standardization of climate-related disclosures in the public sector will influence market expectations and business practices across all sectors, including private companies. Investors and stakeholders may increasingly expect similar levels of transparency and disclosure from private companies.

- Preparation for IPO: Understanding and voluntarily adhering to certain aspects of the SEC's climate disclosure rules can position private companies favorably in case new state, federal or international regulations are extended to them in the future. Additionally, preparing climate reporting in line with the SEC’s rules today will make it easier to prepare for an initial public offering (IPO) and more easily meet listed company readiness.

- Competitive Advantage: Demonstrating proactive engagement in climate-related reporting can provide a competitive advantage to private companies. It can improve their brand reputation and make them more attractive to investors, customers, and partners who prioritize sustainability and environmental responsibility.

- California Climate Rules: Many mid-sized US private companies are likely to be impacted by California’s SB 253 and 261, which will require 10,000 US companies that do business in California to report on their Scope 1, 2, and Scope 3 emissions and climate risks beginning in 2026 regardless of SEC filing status.

How can companies prepare for compliance with the SEC Climate Rule?

With LAFs beginning to report on 2025 data, the compliance timeline is shorter than it may initially seem. Although 98% of the S&P 500 and 90% of Russel 1000 are already reporting some aspects of their climate information, it is more general information about certain physical and transition risks. For most filers, these new rules represent a significant expansion of their current climate reporting, and for others, it is a net new process.

In order to prepare, here are some simple steps toward SEC climate disclosure compliance that you can take now:

Understand your Compliance Requirements

Impacted companies should familiarize themselves with the specifics of the SEC's climate reporting rules, including the disclosures required for their company size. Whether they need to report just material climate risks, if they need to report GHG emissions and get an assurance, and by when.

Assess what parts of this new compliance rule your company is already doing and what additions you might have to make to your climate reporting program to meet these new rules.

Undertake a Materiality Assessment

With materiality being such a key aspect of this rule, conducting a materiality assessment will ensure your company is collecting all relevant material climate risks and emissions. Even beyond SEC reporting, a materiality assessment is a critical starting point for every company embarking on a sustainability journey and helps to frame the relevant topics for action.

If your company needs to update or conduct a first materiality assessment to help determine what should be reported, check out Good.Lab’s materiality software that streamlines multi-user inputs into a visual matrix, and helps you prepare for compliance.

Complete a Climate Risk Assessment

Companies should identify, assess, and manage climate-related risks that could have a material impact on their business, financial statements, or strategy. This includes assessing both physical risks, such as severe weather events, wildfires, and floods, and transition risks, like policy changes or technological shifts. Conducting a climate risk readiness assessment to gauge your reporting capabilities against TCFD guidelines is the best place to start.

Start Collecting Data

Develop or improve strategies for collecting and reporting data on GHG emissions and other climate-related information. Companies may need to invest in new technologies or processes to accurately measure and report Scope 1 and 2 emissions.

If you need help collecting all of your Scope 1 and 2 emissions, check out Good.Lab’s GHG Emissions Calculator to quickly produce your carbon footprint. It will enable you with all of the data and metadata you need to access audit-ready data for conducting any required or voluntary assurances.

Common compliance challenges for the SEC Climate Rule

Many of these climate reporting processes will be new for companies, and they represent complex and potentially costly challenges to get ahead of before disclosure deadlines. The many new systems, processes, and technologies needed to measure emissions accurately, gauge, record, and plant to mitigate climate risks, and create governance structures require certain knowledge, experience and expertise.

The SEC’s original proposals for climate disclosure were estimated to cost $530,000 on average in the first year of disclosure. With the final rule being less rigorous, the SEC still estimates that the costs for compliance will be substantial and could range from less than $197,000 to over $739,000, depending on the extent of reporting. However these costs can be mitigated with an active approach wherein companies take early action and work with a reputable provider with flexible solutions that scale with your companies needs.

Additionally, many companies will find that they lack the in-house expertise to conduct comprehensive climate risk assessments, GHG measurements, and assurances and will need to put plans in place to hire climate experts or partner with third-parties to ensure they mitigate the legal and reputation risks of non-compliance.

Considering what is required by the new SEC climate rules, and the challenges they represent, the best time to start preparing is today. Early adoption will reduce the burden of compliance, when the time to report comes.

Good.Lab’s climate experts are prepared to help your company effectively navigate toward compliance. Reach out to talk about preparing for SEC compliance, conducting a climate risk readiness assessment, a materiality assessment, or measuring emissions today!

FAQs

The SEC’s rule, known as The Enhancement and Standardization of Climate‑Related Disclosures for Investors, was finalized on March 6, 2024 after a 3–2 vote. It requires comprehensive, standardized climate-related reporting from public companies.

Large Accelerated Filers (LAFs) and Accelerated Filers (AFs) must report Scope 1 and Scope 2 greenhouse gas emissions and disclose material climate-related financial risks following TCFD-aligned standards.

Scope 3 emissions must only be disclosed if the company has made public Scope 3 targets or if Scope 3 is financially material. Smaller companies are exempt.

This includes governance, strategy, risk management, climate targets, and transition plans.

2025–2027: LAFs begin reporting climate risks (2026 for FY 2025) and material Scope 1/2 emissions (2027 for FY 2026). AFs follow, with risk reporting in 2028 and emission reporting in 2029.

2030 onwards: LAFs and AFs must obtain limited assurance on emission data (2030 for LAFs, 2032 for AFs), with reasonable assurance required for LAFs by 2034. Smaller filers start risk reporting in 2028 and have delayed assurance obligations.

Material climate risks are those a reasonable investor would deem significant to financial performance. Companies must disclose identification processes, governance structure, quantitative and qualitative impacts, transition plans, internal carbon pricing—or scenario analysis—and impacts on financial statements. Materiality assessments must be conducted ahead of compiling disclosures.

The SEC mandates third-party limited assurance on Scope 1 and Scope 2 GHG emissions disclosures for large companies, progressing to reasonable assurance later.

- Limited assurance (similar to a review) will be required 1 year after emissions disclosure begins.

- Reasonable assurance (similar to a full audit) is required for Large Accelerated Filers starting in 2034.

Assurance is intended to improve data quality and investor confidence, so companies should start building audit-ready processes early.