California’s climate disclosure rules—now consolidated under SB 219 (formerly SB 253 and SB 261)—require companies doing business in the state to disclose their greenhouse gas emissions and climate-related financial risks starting in 2026.

The clock is ticking for ~10,000 companies with over $500 million in revenue doing business in California. Starting in 2026, they’ll be required to disclose their full greenhouse gas emissions and climate-related risks. That makes 2025 the make-or-break year to get your data, teams, and strategy aligned. Here's what’s coming—and how to prepare.

Key Takeaways

- California's climate reporting regulation is now unified under SB 219.

- 2025 is a critical year to prepare data governance practices for streamlined emissions reporting and verification under SB 219.

- SB 219 will impact over 10,000 U.S. companies doing business in California—and even more within their supply chains.

- SB 219 mandates annual reporting and assurance for Scope 1, 2, and 3 emissions, along with biennial climate risk reporting.

What is California SB 219?

In September 2024, California enacted Senate Bill 219, consolidating and amending SB 253 and SB 261. While the core requirements remain intact—mandating that U.S. companies doing business in California disclose climate-related risks and verified greenhouse gas emissions—SB 219 introduced key changes. It gave the California Air Resources Board (CARB) expanded authority to define reporting rules and removed the filing fee for reporting entities. In short: same goals, updated playbook.

So, what exactly is required—and who needs to comply? Whether you're in or near the $500 million revenue threshold, knowing where your company stands under SB 253 and 261 is non-negotiable. These rules are about more than just compliance—they're a signal that climate risk disclosure is becoming standard business practice. Here's a breakdown of what you’ll need to report and who’s on the hook.

CA SB 253: GHG Emissions Reporting

GHG emissions reporting under SB 219, is the same as it was under SB 253. It requires accurate calculations for Scope 1, 2, and 3 emissions reporting in line with the Greenhouse Gas Protocol Corporate Accounting and Reporting Standard and the Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard.

Which businesses are covered by SB 253?

SB 253 applies to U.S.-based corporations, partnerships, and limited liability companies that meet the following criteria as reporting entities:

- Conduct business in California (which includes companies with financial transactions, headquarters, or significant operations in the state)

- Have annual revenues exceeding $1 billion USD (estimated to be 5,400 companies)

What are the key requirements of SB 253?

To meet the requirements of SB 253 (as maintained under SB 219), companies must:

- Report Scope 1 & 2 GHG Emissions: Starting in 2026, companies must publicly report their Scope 1 (Direct emissions) and Scope 2 (Indirect emissions) based on 2025 data.

- Report Scope 3 GHG Emissions: Beginning in 2027, companies must also report their Scope 3 emissions (Indirect emissions from the entire value chain) based on 2026 data.

CARB will set the timeline for Scope 3 reporting in 2027. Under the original SB 253, companies had 180 days after reporting Scope 1 and 2 emissions to submit Scope 3. The updated timeline is expected to give companies additional breathing room to tackle the more complex task of measuring and disclosing Scope 3 emissions.

Data Assurance under SB 253

Companies will also be required to have their GHG emissions data audited by a third party based on the following timeline:

- Limited Assurance: Required for Scope 3 data starting in 2027

The penalties for non-compliance with the GHG emissions reporting side of SB 219 could result in a fine of up to $500,000 per reporting year. The penalties will consider the reporter’s previous compliance efforts and if the reporting was made in good faith. There will also be safe harbors for Scope 3:

- No penalties will be imposed for inaccuracies in Scope 3 emissions reporting, provided that the statements were made on a reasonable basis and in good faith.

- Between 2027 and 2030, penalties related to Scope 3 emissions will only apply to cases of non-submission.

CA 261: Climate Risk Reporting

Climate risk reporting under SB 219 remains consistent with the original requirements of SB 261. It mandates that large businesses operating in California prepare and publish climate-related reports every two years, specifically focused on identifying and addressing climate risks. These reports must cover both physical and transition risks associated with climate change, along with the strategies companies are implementing to mitigate them.

Reporters must follow the Task Force on Climate-related Financial Disclosures (TCFD) framework, which centers on governance, strategy, risk management, and metrics and targets. Companies already reporting under TCFD or ISSB standards can leverage those reports to satisfy SB 219 requirements.

Which businesses are covered by SB 261?

SB 261 applies to U.S.-based corporations, partnerships, and limited liability companies that meet the following criteria as reporting entities:

- Conduct business in California (which includes companies with financial transactions, headquarters, or significant operations in the state)

- Have annual revenues exceeding $500 million USD (estimated to be 10,000 companies)

What are the key requirements of SB 261?

To meet the requirements of SB 261 (as maintained under SB 219), companies must:

- Identify and disclose climate-related financial risks using the TCFD framework, covering physical and transition risks

- Report on the actions and strategies the business is taking to mitigate or adapt to those risks

- Publish the climate risk report publicly on the company’s website

- Submit a formal statement to the California Secretary of State confirming that the disclosure has been completed

- Ensure the report is substantive and complete—inadequate disclosures may result in administrative penalties

- Prepare for third-party review—CARB will partner with a nonprofit climate disclosure organization to evaluate reports for completeness and quality, and to analyze systemic and sector-specific risks

Penalties for companies that fail to publish climate risk reports or insufficient reports are fined up to $50,000 per reporting year. Previous compliance efforts and good faith will be considered when assessing penalties.

Timeline for CA SB 219 Adoption

As of the most recent CARB and Ninth Circuit Court updates on November 18, 2025, the deadline for submitting Scope 1 and 2 emissions data to comply with SB 253 is August 10, 2025.

For SB 261, although the enforcement for the original due date of January 1, 2025 is technically paused until the expedited January appeal, we recommend to continue preparing. We anticipate the stay to be reversed and reports to be due in 2026. As I've written in ESG News, "The most important thing is to keep moving forward. A wait-and-see approach only increases risks of non-compliance.”

How can businesses prepare?

To ensure compliance with SB 219, businesses should take the following steps:

1. Establish ESG Data Governance Practices

Effective ESG data governance keeps your climate data accurate, complete, and audit-ready. Starting in 2025, a solid strategy will make it easier to collect, report, and verify the data required under SB 219. Here's what strong data governance looks like:

- Clearly defined roles: Assign specific roles to ensure relevant data is collected from each team and stored in the centralized data hub. One person will be required to engage different functions to collect data, and a cross-functional team should be developed and regularly meet to go over reporting and data collection processes.

- Centralized data management: Store all your emissions data and any accompanying documentation and metadata in a single, accessible location. This central hub of climate data makes it easier for auditors to report and assess.

- Data quality for verification and audit readiness: Set up processes to routinely validate data quality. This can involve creating a standardized collection process and data templates to ensure consistency. This should be done internally and by an external third party for an interim audit to ensure that limited assurance requirements will be met.

- Supplier data integration: Begin engaging with suppliers to align data collection with SB 219 Scope 3 reporting requirements.

2. Measure Scope 1 and 2 Emissions

In the first year of compliance, you only have to report Scope 1 and 2 emissions, so this should be your first area of focus. In carbon accounting, these are typically the easiest emissions to collect and calculate:

- Scope 1: Direct emissions from sources your company owns or controls, such as facilities and vehicles.

- Scope 2: Indirect emissions from the electricity, steam, heat, or cooling your company purchases.

Reporting companies should already have the data needed to calculate Scope 1 and 2 emissions. In 2025, focus on centralizing and verifying that data to streamline tracking. Or skip the hassle—use Good.Lab’s GHG calculator to make emissions reporting easy.

3. Align with TCFD Reporting

Climate risk reporting under SB 219 is fully aligned with the TCFD framework. Understanding its four core pillars—governance, strategy, risk management, and metrics & targets—is key to meeting the requirements.

SB 219 follows a “report or explain” approach, meaning companies must disclose in line with TCFD as much as possible and explain any gaps, including how they plan to address them. In 2025, use Good.Lab’s Climate Risk Readiness solution to conduct a gap assessment, identify what can be addressed ahead of the first report, and build a roadmap to close remaining gaps before the next cycle in 2028.

4. Engage with Suppliers

SB 219 requires companies to collect data from across their value chains. With the inclusion of Scope 3 GHG emissions and climate risk disclosures tied to the supply chain, reporters will need to request emissions and risk data directly from their suppliers.

While Scope 3 reporting doesn’t begin until 2027, early supplier engagement is critical. Starting now ensures your suppliers will be ready to deliver the data you need—especially their Scope 1 and 2 emissions. If you need support laying this foundation, Good.Lab can help you segment your supplier base and assess readiness to streamline future reporting.

5. Prepare for Limited Assurance

Although attaining limited assurance is not required in 2026 for Scope 1 and 2 emissions, we would still recommend it as the most advisable path for companies. Strong data governance is a must—emissions data and supporting metadata need to be organized, accurate, and stored in a central location that auditors can easily access. A pre-audit check ahead of the compliance deadline is key to identifying and closing data gaps early.

Good.Lab’s carbon data management platform simplifies this process, offering centralized storage and downloadable reports to streamline assurance.

Also, limited assurance will be required for Scope 3 in 2027. Now is the time to lay the foundation for audit-ready emissions data.

SB 219 and the Global Shift Toward Aligned Climate Disclosure

California’s SB 219 is part of a broader global movement toward consistent, high-quality climate disclosure. Its requirements closely align with major international frameworks, including the International Sustainability Standards Board (ISSB) Standards and the EU’s Corporate Sustainability Reporting Directive (CSRD). All emphasize Scope 1 and 2 emissions reporting and climate risk disclosure based on the TCFD framework. Most, including SB 219 and CSRD, also require third-party assurance.

While there are differences in scope and applicability, the alignment around foundational standards like the GHG Protocol and TCFD signals a clear trend: global climate reporting is converging—and consistency is no longer optional.

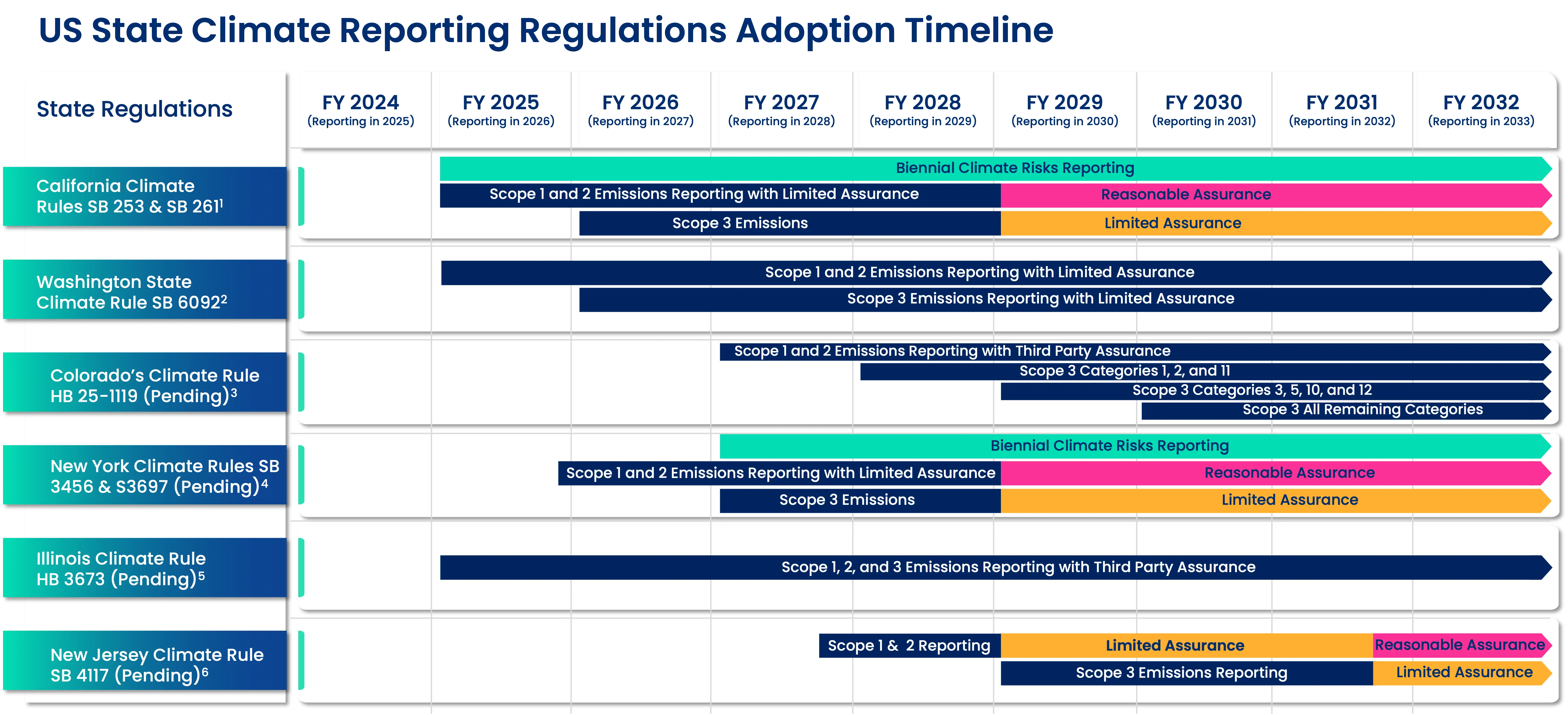

Other U.S. States Following California’s Lead

California’s SB 219 has set the pace for climate disclosure in the U.S.—and other states are quickly catching on. New York, Illinois, and Washington have all introduced climate risk and emissions reporting legislation modeled after California’s approach, signaling a growing push for state-level action.

- New York: SB S897A (Climate Corporate Accountability Act) would require companies with over $1 billion in annual revenue to report—and obtain assurance—on their Scope 1, 2, and 3 emissions, starting two years after enactment. SB 5437 would add annual climate risk reporting.

- Illinois: HB4268 mandates annual disclosure and third-party verification of Scope 1, 2, and 3 emissions for companies with over $1 billion in revenue, starting January 1, 2025.

- Washington: SB 6092 (Climate Corporate Data Accountability Act) proposes GHG reporting and assurance for large businesses beginning in 2026, with Scope 3 reporting required starting in 2027.

If these proposals become law, here’s how the timeline would play out:

Looking ahead

You could wait until 2026 to start your SB 219 reporting—but by then, you’ll be playing catch-up. Many of the required data points, like Scope 3 spend-based emissions, rely on historical inputs. Whether you start now or later, you'll be looking backward. The real question is: Do you want to get your first reps in while you still have time—or under the pressure of a deadline?

Companies that start in 2025 will be better prepared to meet the emissions assurance and climate risk disclosure requirements without last-minute scrambles. Early action gives you time to build reliable data systems, strengthen supplier collaboration, and uncover the gaps—like governance disclosures, risk mapping, or target-setting—that most companies only find once they begin the process.

And it’s not just about California. The data and assurance work you do for SB 219 can be reused for other regulatory regimes like the CSRD, ISSB, and emerging U.S. state-level rules. By starting now, you’re reducing duplication and future-proofing your compliance approach.

Ready to get ahead? Talk to Good.Lab’s experts and start your 2025 roadmap to confident, audit-ready compliance.

Good.Lab can help

Good.Lab provides sustainability software and consulting services to help companies meet their climate disclosure obligations with confidence.

With our solutions, you can:

- Conduct a thorough assessment of your carbon footprint

- Prepare for climate risk reporting with readiness assessments and actionable roadmaps

- Reach full compliance with California’s SB 219 requirements

- Ensure your sustainability data is accurate, auditable, and third-party verified before disclosure

FAQs

SB-219 merges California’s earlier climate disclosure laws (SB 253 and SB 261) into a single, comprehensive regulation. It significantly expands corporate obligations for greenhouse gas emissions reporting and climate risk disclosures.

The law applies to more than 10,000 companies doing business in California. Companies with over $1 billion in annual revenue must report Scope 1 and Scope 2 emissions beginning in 2026, with Scope 3 reporting starting in 2027. Companies with over $500 million in revenue must disclose climate-related financial risks starting in 2026.

Companies must annually report Scope 1 and Scope 2 greenhouse gas emissions, followed by Scope 3 emissions from 2027 onward. In addition, they must publish biennial climate-related financial risk reports aligned with the TCFD framework, addressing both physical and transition risks.

Limited assurance for Scope 1 and 2 emissions begins in 2026, transitioning to reasonable assurance in 2030. Scope 3 assurance will phase in later. Penalties can reach up to $500,000 per year for emissions-related violations and $50,000 for inadequate climate-risk disclosures, although good-faith errors are not penalized.

Businesses should start in 2025 by setting up robust data governance processes, centralizing systems for emissions measurement, engaging cross-functional teams for data ownership, and preparing climate risk disclosures that align with the TCFD framework.