Decoding the EU’s ESG Regulations: What U.S. Companies Need to Know

Ted Grozier

Principal & Chief Sustainability Officer

Ted is a consultant and project manager who is expert at turning ESG innovation into business success. He was an Engagement Manager at GreenOrder, the pioneering consulting firm that Fortune called the “go-to guys for green business.”

He also served as Flagship Manager for EIT Climate-KIC, the European Union’s largest climate innovation initiative, in Berlin, Germany, where he lived for eight years. Ted is a Harvard engineer with an MBA from the Tuck School of Business at Dartmouth.

The European Union (EU) has created one of the most ambitious and progressive green agendas globally. The EU ESG regulatory landscape extends far beyond most other regions, as they aim to meet the goals set out in the Green Deal.

Among the more ambitious goals of the EU’s Green Deal, the bloc plans to be the first climate-neutral continent by 2050, with interim goals of reducing emissions by 55% by 2030 and 90% by 2040.

To meet these lofty goals, the EU has proposed and, in some cases, already implemented a swathe of ESG regulations and standards to ensure the companies contributing to the EU’s carbon footprint, water use, biodiversity loss, and social issues are both documenting their impacts, reporting them, and reducing them.

Read on to decode the confusing alphabet soup that has been created across the EU’s ESG regulatory landscape. In this article, we’ll explore the implications and insights of the four main EU ESG acronyms, EFRAG (European Financial Reporting Advisory Group), CSRD (Corporate Sustainability Reporting Directive), ESRS (European Sustainability Reporting Standards), and the CSDDD (Corporate Sustainability Due Diligence Directive), as well as provide an overview of other notable regulations to know and their relevance to medium-sized US companies.

A Deep Dive into EU ESG Regulations

Public support, political will, and ambitious targets have meant that the EU has a long history of being a global frontrunner in implementing sustainability regulations. Since 2020, the pace at which these far-reaching ESG regulations have been proposed has increased exponentially.

In 2014, the EU released its first foray into mandated climate and ESG reporting with the Non-Financial Reporting Directive (NFRD). The NFRD required publicly listed companies with over 500 employees (~10,000 companies) to produce annual sustainability reports, which include information about the companies’ impact on the environment and society. However, investors and other stakeholders found the scope of the NFRD insufficient, and the sustainability information reported unreliable.

The European Financial Reporting Advisory Group (EFRAG) creates regulations and accounting standards for the EU Commission, including sustainability reporting regulations and standards. It was set up to advise the EU on their ESG reporting, suggested that the EU update the NFRD with the CSRD, which widens the scope of the ESG metrics that companies will have to disclose and the number of companies that are required to report. The EFRAG also created the ESRS, which determines what, when, and how to disclose to be compliant with the CSRD.

The EU Parliament also approved another piece of extensive ESG regulation, the CSDDD or CS3D, which makes companies identify, reduce, and mitigate impacts on the environment, labor and human rights, and governance across companies’ operations and global supply chains.

EFRAG

The European Financial Reporting Advisory Group, or EFRAG, differs from the other acronyms in that it is not a disclosure regulation. Instead, it was the group set up to create the regulations and standards. It was created in 2001 to help the EU Commission to develop accounting standards. More recently, their remit has expanded to developing the EU’s sustainability reporting standards, firstly the NFRD and then the CSRD and ESRS. EFRAG’s work has centered around creating a holistic set of sustainability reporting regulations that are comparable and compatible with companies across the EU and in alignment with other global reporting standards, such as the Global Reporting Initiative (GRI) and the International Sustainability Standards Board (ISSB).

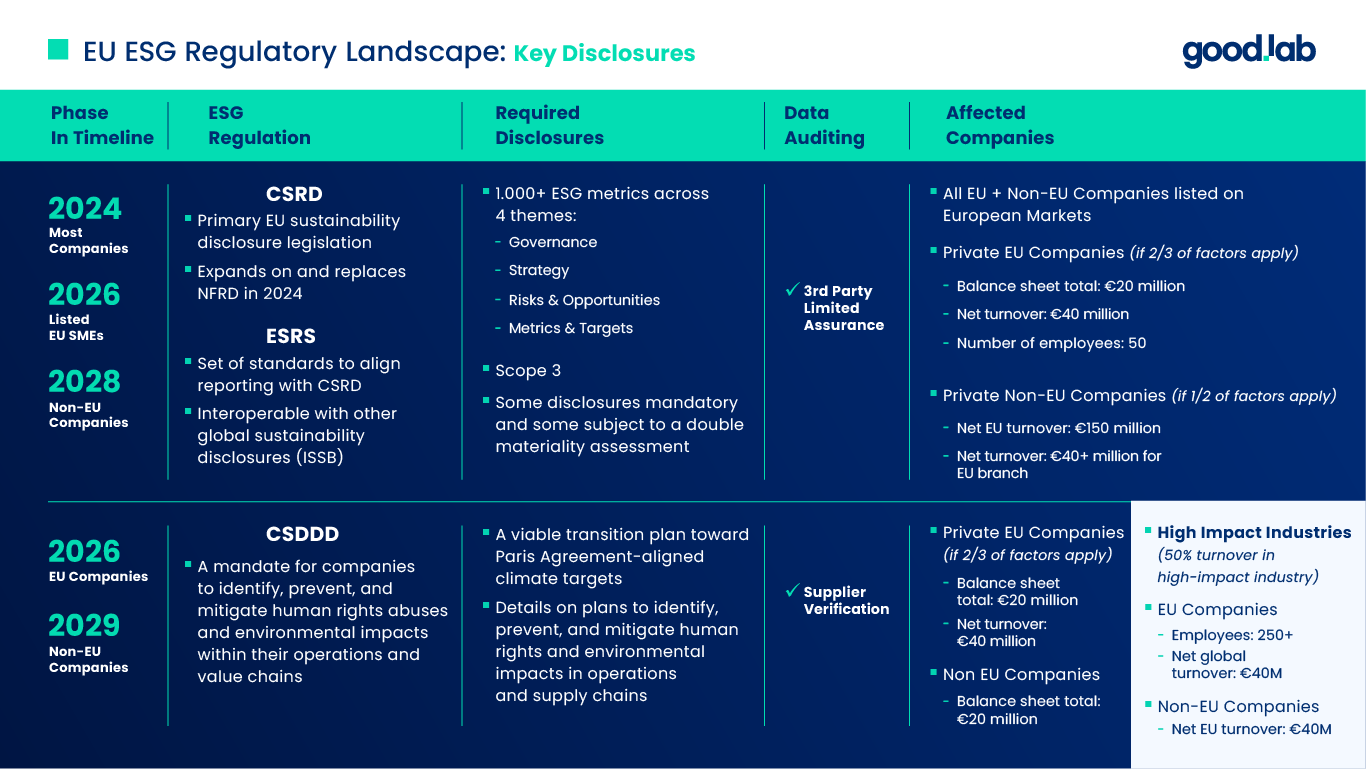

CSRD

Purpose: The CSRD replaced the NFRD starting in 2024, marking significant progress in the EU’s sustainability reporting landscape and introducing the world’s most comprehensive reporting legislation to date. Reporting will require affected companies to disclose information on more than 1000 ESG performance metrics. These metrics encompass various aspects, including the social and environmental impact of companies and their value chains. CSRD reporting importantly includes the reporting of scope 3 emissions, 3rd party limited assurance on the contents of their reporting, and will include penalties for non-compliance, to be decided by member states at the latest by July 6th, 2024. France has already indicated that non-compliance could result in criminal charges.

Scope: The CSRD will affect a total of 50,000 EU companies, and 11,000 non-EU companies (including 3,000 US companies) that fall under its purview. This includes every listed EU company, even small and medium-sized enterprises (SMEs), and any EU company exceeding the limits of at least two of the three following thresholds:

Balance sheet total: €20,000,000

Net turnover: €40,000,000

Number of employees: 50 employees

The CSRD will also affect any non-EU company that is either listed on any EU-regulated market or satisfies either of these two criteria:

Net turnover: €150 million euros in the EU

EU branch net turnover: greater than €40 million euros

It is worth noting that non-EU companies would be expected to report the sustainability information that covers their entire company, not just the EU part of the company.

Timing: Companies impacted by the CSRD will have to make their first reporting 2025 for FY 2024, starting with the largest companies, followed by smaller listed companies in 2026, and non-EU companies won’t be expected to disclose till 2028.

ESRS

Purpose: The ESRS is the reporting standards that should be followed when reporting to the CSRD. The ESRS is basically the tool used to achieve compliance with the CSRD. The original proposals for the ESRS were developed by EFRAG to give companies guidance and methods for consistent and comparative reporting. The ESRS standards were modified by the EU Commission after the EFRAG proposals to make much reporting not mandatory but subject to a materiality assessment and to make them interoperable with other global sustainability disclosure standards, such as those in development, by the International Sustainability Standards Board (ISSB).

Scope: Any company that falls under the CSRD, must use the ESRS for sustainability reporting.

Timing: Companies will start using the ESRS to comply with CSRD between 2024 and 2028.

CSDDD

Purpose: In 2023, the EU Parliament agreed to introduce the CSDDD. The primary objective of the CSDDD is to ensure that companies exercise due diligence throughout their operations and supply chains. It will mandate companies to identify, prevent, and mitigate adverse human rights and environmental impacts within their value chains and make companies create a viable transition plan toward Paris Agreement-aligned climate targets. Companies will be expected to disclose how they are meeting the CSDDD in annual reports, and non-compliance could lead to fines to both the company and, uniquely, company executives too.

Scope: Like the CSRD, the CSDDD will affect both EU and non-EU companies. However, with the CSDDD, the rules will apply to two groups of companies. The first groups are large companies. The second group is smaller companies in high-impact sectors, which includes approximately 4,000 non-EU companies and 12,800 EU companies across both groups. For the rules to apply, companies need to meet the following thresholds:

EU (Group1): Companies with more than 500 employees and €150 million of net worldwide turnover

Non-EU (Group 1): Companies with more than €150 million of net turnover in the European Union

EU (Group 2): Companies with more than 250 employees and €40 million of net worldwide turnover, if at least 50% of such turnover is generated in a high-impact industry, such as manufacturing, extraction and trade of mineral resources, agriculture, forestry, etc.

Non-EU (Group 2): €40 million of net turnover in the European Union if at least 50% of such turnover is generated in one of the high-impact sectors mentioned above

Timing: The CSDDD is yet to be finalized, but if approved, it will be phased in for EU companies in 2026 and non-EU companies in 2029.

Other Important EU ESG Regulations to Know

Sustainable Finance Disclosure Regulation (SFDR)

The SFDR is designed specifically for ESG disclosures in financial institutions. It requires asset managers, investment funds, insurers, and other financial institutions to report information regarding how they integrate ESG factors into their investment decisions and how the impact of ESG on financial products. The SFDR divides financial products into three categories, each with varying disclosure requirements:

Article

Description

Disclosure Requirements

6

Funds with no ESG scope

How sustainability risks are considered in the fund

8

Funds that promote environmental or social characteristics

Information on how the fund promotes environmental or social characteristics

9

Funds that have sustainable investment as their objective

Information on how the fund is aligned with its objective

Table 2 – SFDR Disclosure Requirements

EU Green Taxonomy

The EU Green Taxonomy works as a way for investors, companies, and policymakers to determine whether a financial activity is sustainable or not. It sets out clear criteria that economic activities must meet to be labeled as environmentally sustainable. Each economic activity must have a sustainable objective to be classed as sustainable to help investors make more informed decisions on sustainable investments.

Green Claims Directive

The Green Claims Directive came into effect in 2023. It effectively prohibits companies from “greenwashing.” It details specific ways products can advertise and market green claims, ensuring any environmental or social claim is substantiated by accurate and transparent data. The Directive will affect any EU or non-EU company making green claims to EU consumers.

Proposal for a Regulation on Public Procurement and Mutual Recognition of Environmental Labelling (PPMFLR)

The PPMFLR is a proposal from the EU to prohibit any products made using forced labor from being sold in the EU. The proposal, which is expected to be finally adopted in 2025, will enforce the withdrawal and punishments for any products created domestically or imported found to have used forced labor.

The Impact of EU ESG Regulations on US Companies

Some may think that these rules will not affect those outside the boundaries of the EU. However, they would be wrong. The EU’s CSRD and CSDDD will affect 11,000 and 4,000 foreign companies, respectively. In the case of the CSRD, over 3,000 US companies publicly listed in the EU or with a large branch or subsidiary in the EU will be affected.

Considering the CSRD includes the disclosure of scope 3 emissions and other sustainability impacts in the value chain, and the CSDDD is focused on identifying, preventing, and mitigating companies’ ESG impacts across their supply chains. Global companies, including US companies, will be responsible for sharing extensive sustainability information with the companies they supply to in the EU.

Whether directly or indirectly, EU regulations will force many companies across the US to disclose their emissions and other ESG metrics.

With so many EU companies affected by the CSRD and the CSDDD and the inclusion in both of value chain sustainability and scope 3 data reporting, US companies that do business or supply companies in the EU can expect contracts from EU companies to include language addressing compliance with these two regulations.

Additionally, with all of the US companies having to meet EU requirements, and the inclusion of scope 3 and other value chain sustainability factors, US SMEs will be more directly affected. And, with the EU pushing the global ESG disclosure regulatory agenda forward, it is possible the SEC could be forced to include scope 3 and eventually other ESG metrics.

Therefore, it is of the utmost importance for companies to start measuring their ESG factors today. Starting now will help companies keep contracts with their largest publicly traded customers, who are most immediately affected by the EU’s and other disclosure regulations, and could help them build a competitive advantage to win new ones. It will also help private companies assess ESG risk in their own operations and value chain and could allow them access to European markets.

Private companies should prioritize their ESG programs and evaluate if they collect the necessary data to meet the compliance requirements of the EU’s regulations. Failing to do so can result in missed opportunities and hinder their growth potential.

US SMEs will have to start considering the ESG disclosure requirements of the EU’s regulations to access European markets and remain competitive.

A Look at US ESG Regulations

In the US, ESG regulations are moving at a much slower pace. Currently, the SEC climate disclosure regulation proposal, which was released in March 2022, is not expected to be finalized until March 2024or possibly later. California’s climate disclosure rules SB 253 & 261 won’t be implemented until 2026 at the earliest. While the final contents of the California rules are not likely to change the final version and scope of the SEC’s rule is still unknown. The main sticking point is whether the disclosure rules will include reporting of scope 3. However, this is largely a moot point, as a substantial amount of the companies covered by the SEC’s regulation will be covered by the California rules and the CSRD, which both already include scope 3. EU lawmakers communicated with the SEC that if their disclosure regulation goes most of the way toward the disclosure requirements of the CSRD, such as including scope 3, US companies would not be required to report to the EU through the CSRD.

With so many US companies affected by some EU regulations and the wider EU regulatory landscape becoming the gold standard for global sustainability disclosure standards, it is likely that most jurisdictions, including the US, will eventually replicate the EU standards.

Early adopters will be able to prepare for any future compliance and take advantage of any other benefit, such as access to new markets, improved brand reputation, and operational efficiencies that come with creating a robust ESG program.

To help you navigate this complex landscape and comply with an ever-growing amount of EU ESG regulations our sustainability experts are ready to help ensure you are compliant. Let’s talk ESG!

FAQs

Yes, if a U.S. company operates in the EU or meets turnover thresholds, it must comply with CSRD and CSDDD, regardless of physical presence in the region.

CSRD focuses on sustainability reporting requirements, while CSDDD mandates companies to perform due diligence on environmental and human rights risks across their operations and value chains.

The European Sustainability Reporting Standards (ESRS) define what, when, and how companies report under CSRD. They ensure data is consistent, comparable, and aligned with global frameworks.

Non-EU companies impacted by CSRD must begin reporting in 2028 for the fiscal year 2027, if they meet the criteria, like significant EU turnover or market listings.

Even if not directly regulated, U.S. SMEs in EU supply chains may face data-sharing demands from EU partners seeking compliance with scope 3 and due diligence rules.

Non-compliance may result in penalties, including fines and possible criminal charges, depending on the EU member state’s enforcement policy and the regulation’s specific requirements.

Disclaimer: Good.Lab does not provide tax, legal, or accounting advice through this website. Our goal is to provide timely, research-informed material prepared by subject-matter experts and is for informational purposes only. All external references are linked directly in the text to trusted third-party sources.

Ted Grozier

Principal & Chief Sustainability Officer

Ted is a consultant and project manager who is expert at turning ESG innovation into business success. He was an Engagement Manager at GreenOrder, the pioneering consulting firm that Fortune called the “go-to guys for green business.”

He also served as Flagship Manager for EIT Climate-KIC, the European Union’s largest climate innovation initiative, in Berlin, Germany, where he lived for eight years. Ted is a Harvard engineer with an MBA from the Tuck School of Business at Dartmouth.

Ready to elevate your sustainability efforts?

Connect with our sustainability experts today!

From sustainability program development to target setting, data management, and reporting, our team can help you fast-track building a world-class sustainability program.

CDP Reporting for Manufacturers: What to Do When a Customer Asks

The CDP portal opened on April 27th. If you received a customer request to disclose and you’re not sure what to do with it, here’s what you need to know. In 2025, of the 23,100+ companies who reported through CDP’s Supply Chain program, more than a third were manufacturers. And more than half of those […]

Customer Asked for Your EcoVadis Score? Here’s What That Means for Your Manufacturing Business

Perhaps the email asking for your EcoVadis score came from your customer’s procurement team, or you found it buried in a supplier onboarding form. Either way, it’s sitting in your inbox, and you’re not sure what to do with it. If you’re wondering what receiving an EcoVadis request as a manufacturer means for your business, […]

State Climate Reporting Laws: A Guide to US Climate Disclosure Laws

Federal climate disclosure rules may be stalled, but state climate reporting laws are not – and for large companies operating across the US, the compliance clock is already running. The situation is more manageable than it looks. Most state rules are built from the same blueprint: California moved first, and every state that followed used […]

Welcome to Good.Lab! We're glad you're here and want you to know that we respect your privacy and your right to control how we collect and use your personal data. Please read our Privacy Policy to learn about our privacy practices or to exercise control over your data.