Takeaways from the inaugural IFRS Sustainability Symposium

Ted Grozier

Principal & Chief Sustainability Officer

Ted is a consultant and project manager who is expert at turning ESG innovation into business success. He was an Engagement Manager at GreenOrder, the pioneering consulting firm that Fortune called the “go-to guys for green business.”

He also served as Flagship Manager for EIT Climate-KIC, the European Union’s largest climate innovation initiative, in Berlin, Germany, where he lived for eight years. Ted is a Harvard engineer with an MBA from the Tuck School of Business at Dartmouth.

Last week’s inaugural IFRS Sustainability Symposium in Montreal convened stakeholders from 18+ countries representing top performing companies, ESG-focused investors, and industry advisors to discuss emerging issues related to sustainability disclosure, including the direction of the IFRS Sustainability Disclosure Standards.

The event covered the following topics across various sessions:

updates on Sustainability Disclosure Standards being developed via IFRS’ standard-setting board — the International Sustainability Standards Board (ISSB)

how IFRS aims to satisfy investor demands for ESG performance data that is high-quality, transparent, reliable, and comparable

panels on the use and uptake of standards being set by the IFRS Sustainability Disclosure and SASB

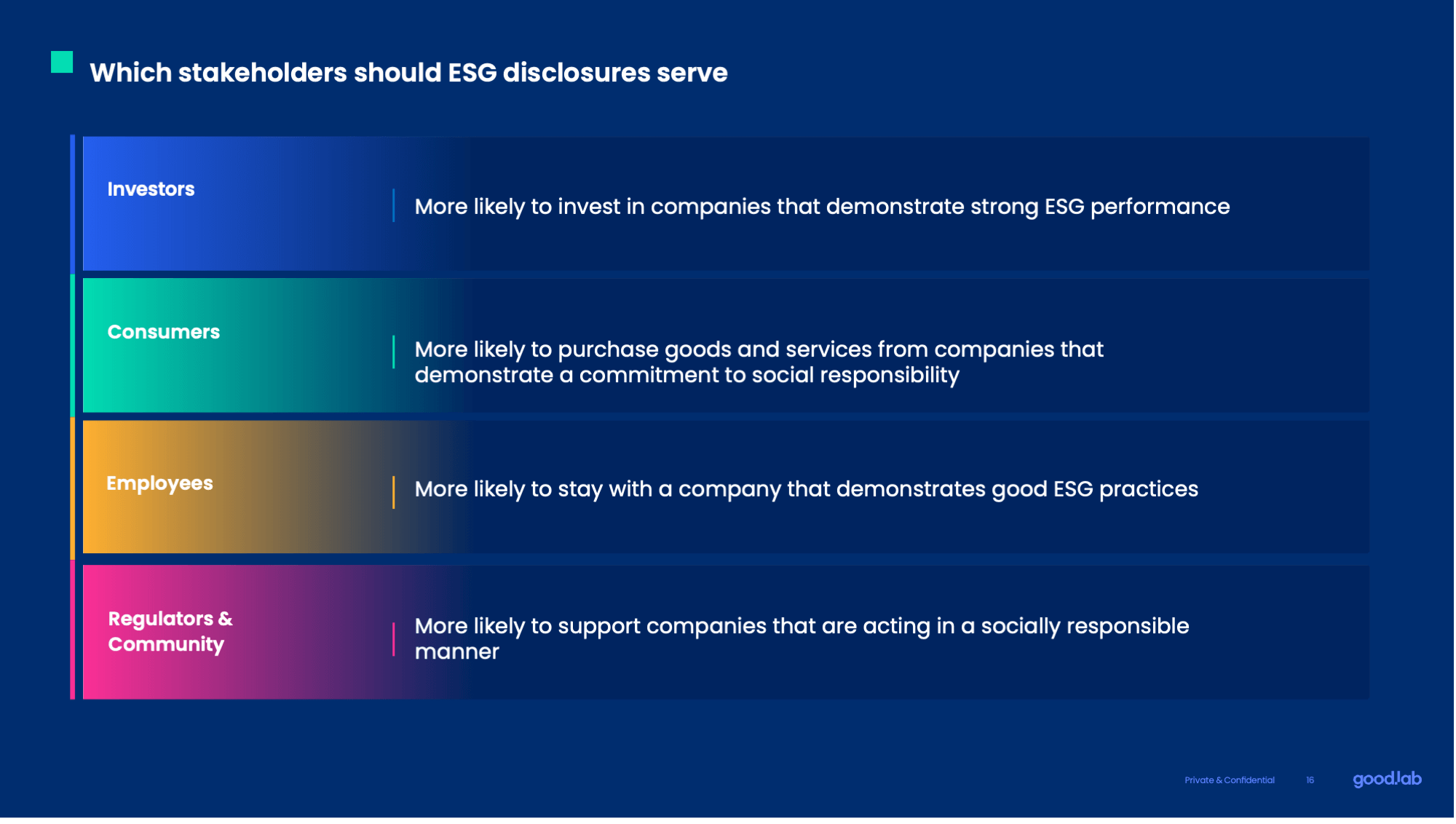

A key theme that came up is which stakeholders should be considered in the broad lens of ESG and how this relates to corporate ESG performance data reporting. Experts weighed in on the important question of stakeholders and the technical content of the standards.

Better ESG disclosures on the horizon

During Symposium is was announced that the sustainability and climate reporting standards will be issued at the end of Q2 2023. They will become effective as of January 2024, meaning businesses would collect sustainability information for the 2024 calendar year and report in 2025.

Whether or not certain provisions are in or out of the standards, when they take effect, etc., are much less important than the trend toward disclosure of climate-related risks and performance.

Regarding the standards, the general tone was that ESG disclosures should be “climate-first, but not climate-only” indicating growing importance of quantifying and improving on social and governance initiatives in addition to climate-related performance. The ISSB plans to address ESG issues not covered in the climate and general sustainability standards at its next board meeting in September.

Climate-related risks, and opportunities

The proposed IFRS S2 (climate-related risks and opportunities) is the least-met part of TCFD today. Companies should look at this as an opportunity to highlight their strengths, not just a burden to report risks. The opportunity is vast for new avenues of value creation driven by potential new revenue from the growing demand for low emissions products and services, as well as the potential for better competitive advantage in light of shifting consumer preferences.

Scope 3 continues to confound

Among attendees, there was broad consensus on Scope 1 and 2 emissions reporting, but concern about getting Scope 3 right. Questions ranged from which categories, when and how to use estimates, and having an extra year to comply. On the flip side, uncertainty is not unique to Scope 3 and ESG reporting and the accounting profession deals with uncertainty all the time. The IFRS will be introducing a framework for how an entity measures its Scope 3 GHG emissions and steps to improve data collection over time. Even with the challenges in measuring Scope 3 emissions, the category still holds potential to prevent some of the worst impacts of climate change. Companies should move ahead to establish a baseline GHG inventory using tools that align to the GHG Protocol Scope 3 Standard.

A final theme that emerged was in relation to the IFRS goal to provide “decision-useful” disclosure for investorsand other capital market participants. The aim of reporting on companies’ ESG and climate-related risks is to help investors make informed decisions. Investor stakeholders are not necessarily the same stakeholders as society at large which includes investors, and shareholders, employees, customers, suppliers, regulators, and the broader community. These stakeholders all have an interest in a company’s ESG performance and can be affected by their decisions.

Toward an integrated reporting model?

The focus on decision-useful information for investors raises the question of how other stakeholders’ needs are considered. Should we instead be moving to an integrated mode of thinking about ESG, e.g., an integrated reporting model? The question may in fact miss the point, as long-term value creation requires a consideration of all stakeholders and all capitals – including financial, manufactured, intellectual, human, social and natural. That is, information that informs the investor about long-term value is by its very nature a form of integrated reporting.

The lively discussions on whether or not certain provisions are in or out of the standards, when they take effect, etc., are much less important than the trend toward disclosure of climate-related risks and performance. Importantly, the IFRS Sustainability Symposium heralded its leadership on the global trend toward greater transparency on the financial implications of climate risk and opportunity and we are happy to be on the forefront of this business transformation.

Disclaimer: Good.Lab does not provide tax, legal, or accounting advice through this website. Our goal is to provide timely, research-informed material prepared by subject-matter experts and is for informational purposes only. All external references are linked directly in the text to trusted third-party sources.

Ted Grozier

Principal & Chief Sustainability Officer

Ted is a consultant and project manager who is expert at turning ESG innovation into business success. He was an Engagement Manager at GreenOrder, the pioneering consulting firm that Fortune called the “go-to guys for green business.”

He also served as Flagship Manager for EIT Climate-KIC, the European Union’s largest climate innovation initiative, in Berlin, Germany, where he lived for eight years. Ted is a Harvard engineer with an MBA from the Tuck School of Business at Dartmouth.

Ready to elevate your sustainability efforts?

Connect with our sustainability experts today!

From sustainability program development to target setting, data management, and reporting, our team can help you fast-track building a world-class sustainability program.

CDP Reporting for Manufacturers: What to Do When a Customer Asks

The CDP portal opened on April 27th. If you received a customer request to disclose and you’re not sure what to do with it, here’s what you need to know. In 2025, of the 23,100+ companies who reported through CDP’s Supply Chain program, more than a third were manufacturers. And more than half of those […]

Customer Asked for Your EcoVadis Score? Here’s What That Means for Your Manufacturing Business

Perhaps the email asking for your EcoVadis score came from your customer’s procurement team, or you found it buried in a supplier onboarding form. Either way, it’s sitting in your inbox, and you’re not sure what to do with it. If you’re wondering what receiving an EcoVadis request as a manufacturer means for your business, […]

State Climate Reporting Laws: A Guide to US Climate Disclosure Laws

Federal climate disclosure rules may be stalled, but state climate reporting laws are not – and for large companies operating across the US, the compliance clock is already running. The situation is more manageable than it looks. Most state rules are built from the same blueprint: California moved first, and every state that followed used […]

Welcome to Good.Lab! We're glad you're here and want you to know that we respect your privacy and your right to control how we collect and use your personal data. Please read our Privacy Policy to learn about our privacy practices or to exercise control over your data.