Andries has had a variety of consulting and management roles throughout his career. He has worked with fast-scaling clients across three continents. Prior to founding Good.Lab, Andries led the blockchain practice at Armanino, a top 20 public accounting firm, was CEO at The Brenner Group, a boutique Silicon Valley financial services firm, and was a partner at Moore Stephens in Shanghai. He started his career at PricewaterhouseCoopers.

Andries holds his B.S. in International Politics from Ghent University in Belgium, an MBA from Binghamton University and founded and participated in the Moore Comprehensive Executive Leadership Program at Harvard Business School.

The recently released International Sustainability Standards Board (ISSB) reporting standards for sustainability and climate-related disclosures marks a huge milestone in the evolution of global ESG and sustainability reporting.

The standards are the culmination of a multi-decade effort to help companies integrate sustainability impacts into their finances, bringing order to the messy landscape of ESG disclosure standards and frameworks. Between 110,000 and 130,000 companies are expected to use the ISSB standards for their corporate reporting and welcome a globally consistent standard as the heralded end to ESG survey disclosure fatigue. For investors, the standards promise to provide comparable data to fully understand the sustainability-related risks and opportunities companies face and accordingly to allocate capital.

For an in-depth look at the contents of the ISSB standards, how they came to be, who will be affected and when, what disclosures are included, and how your company can efficiently align to these reporting standards, read on.

Getting to a Global ISSB Reporting Standard

The ISSB was formed by the International Financial Reporting Standards (IFRS) in 2021 at COP26 in Glasgow to unify climate and ESG reporting under one global standard. The ISSB brings together the responsibilities of the Climate Disclosure Standards Board (CDSB), Value Reporting Foundation (VRF), the International Integrated Reporting Council (IIRC), and the Sustainability Accounting Standards Board (SASB).

More recently, the ISSB earned the support of the International Organization of Securities Commissions (IOSCO), G7, G20, and global investment community. We also anticipate further alignment with the Task Force on Climate-Related Financial Disclosures (TCFD) and Carbon Disclosure Project (CDP) reporting in 2024. The Global Reporting Initiative (GRI) may also merge with the ISSB eventually, according to CEO at GRI, Eelco van der Enden.

The ISSB has collaborated with regulators in various regions, including the US and EU, to ensure that disclosures are consistent and compatible with the SEC’s upcoming climate disclosure regulation and the EU’s Corporate Sustainability Reporting Directive.

The four key objectives of the ISSB are to:

Develop standards for a global baseline of sustainability disclosures

Meet the needs of investors for comparable, compatible, and useful sustainability information

Enable companies to provide comprehensive sustainability information to global capital markets

Facilitate interoperability with disclosures that are jurisdiction-specific and/or aimed at broader stakeholder groups

Who Will be Affected by the ISSB Reporting Standards

Mandated ISSB Reporting by Public Companies

Global financial regulators, such as the SEC in the US, are starting to implement rules that will make publicly traded companies, and in some rare cases private companies, share climate and sustainability information in their annual financial reports. The ISSB reporting standards will likely be the basis or at least be interoperable with these new ESG reporting mandates.

A month after their release, the ISSB standards received endorsement from the International Organization of Securities Commissions (IOSCO), the global security regulator body representing 95% of global capital markets. This means that global regulators support the standards as the global baseline for sustainability-related disclosures. IOSCO Chair Jean-Paul Servais expects as many as 130,000 companies to use the ISSB standards eventually.

Countries, including the UK, Singapore, Canada, and Japan, have already agreed to base their sustainability disclosure regulations for publicly traded companies on the ISSB standards and could require reporting as early as 2025. Other sustainability reporting mandates from the EU’s Sustainability Reporting Standards and U.S. SEC’s Climate Disclosure Regulation have been designed to ensure interoperability with the ISSB standards.

The ISSB standards were designed to ensure companies can easily integrate sustainability-related information in financial statements, such as 10-Ks. Therefore, it is most likely that the ISSB reporting standards will just become another facet of financial reporting.

Whether sustainability-related reporting regulations are based on the ISSB Standards or are meant to be interoperable with them, global sustainability disclosure regulations will use the ISSB standards as a baseline.

ISSB Reporting Standards and the SEC

As the SEC’s Climate Disclosure Rule for US public companies is anticipated to be implemented by the end of 2023, US-based companies are preparing to disclose climate-related risks and opportunities facing their businesses.

The ISSB Standards and the SEC Climate Disclosure Rule are similar in how they were developed, having both been based on the four reporting themes of the TCFD. However. Despite the similarities, the ISSB requirements for disclosure information are significantly more demanding than those of the SEC.

The ISSB mandates the inclusion of additional sustainability-related details and scope 3 information, which may or may not be included in the final SEC climate disclosure ruling.

Even though the ISSB’s reporting standards require more stingent reporting than the SEC’s climate disclosure, many companies have said they intend to voluntarily use the ISSB standards over the SEC.

The promise of voluntary sustainability disclosures, which are comparable and consistent across jurisdictions with the ISSB, is more appealing to some companies than waiting to see what the SEC release. The global market is aligning with the ISSB standards and US companies don’t want to get left behind.

While the ISSB Standards will be optional for most private companies, many will still feel pressure from their investors, customers, and other stakeholders to report on their sustainability and ESG data.

Requests from the CDP are just the tip of the iceberg as soon as large publicly traded companies are affected by ISSB standards-based regulations that include scope 3 emissions and other sustainability metrics in the value chain. Most private companies across the global economy will begin to receive requests for information from their buyers and will need to comply to maintain business standing.

As the de facto standard for reporting that is interoperable with almost every other ESG and sustainability reporting mechanism that exists today, companies that align in advance to the ISSB standards will save themselves time and resources.

Private companies that adopt the ISSB standards early can expect the following benefits:

Improved competitive advantage: With the world’s largest companies expected to align their ESG reporting to the ISSB, they will likely expect their suppliers and other companies in their value chain to report using the same standard. Early adopters signal to their customers that they are willing to make a commitment to sustainability and help the buyers achieve their own goals.

Getting a handle on climate and ESG risks: The ISSB standards provide a structured approach to identifying, assessing, and managing sustainability-related risks and opportunities. This can help companies quantify the potential physical and transition risks and opportunities they may face in order to create strategies to build resiliency.

Ability to attract investment: By aligning to the ISSB reporting standards, companies make their ESG performance comparable, enabling them to attract investors, considering the increased focus on ESG factors in today’s investment decisions.

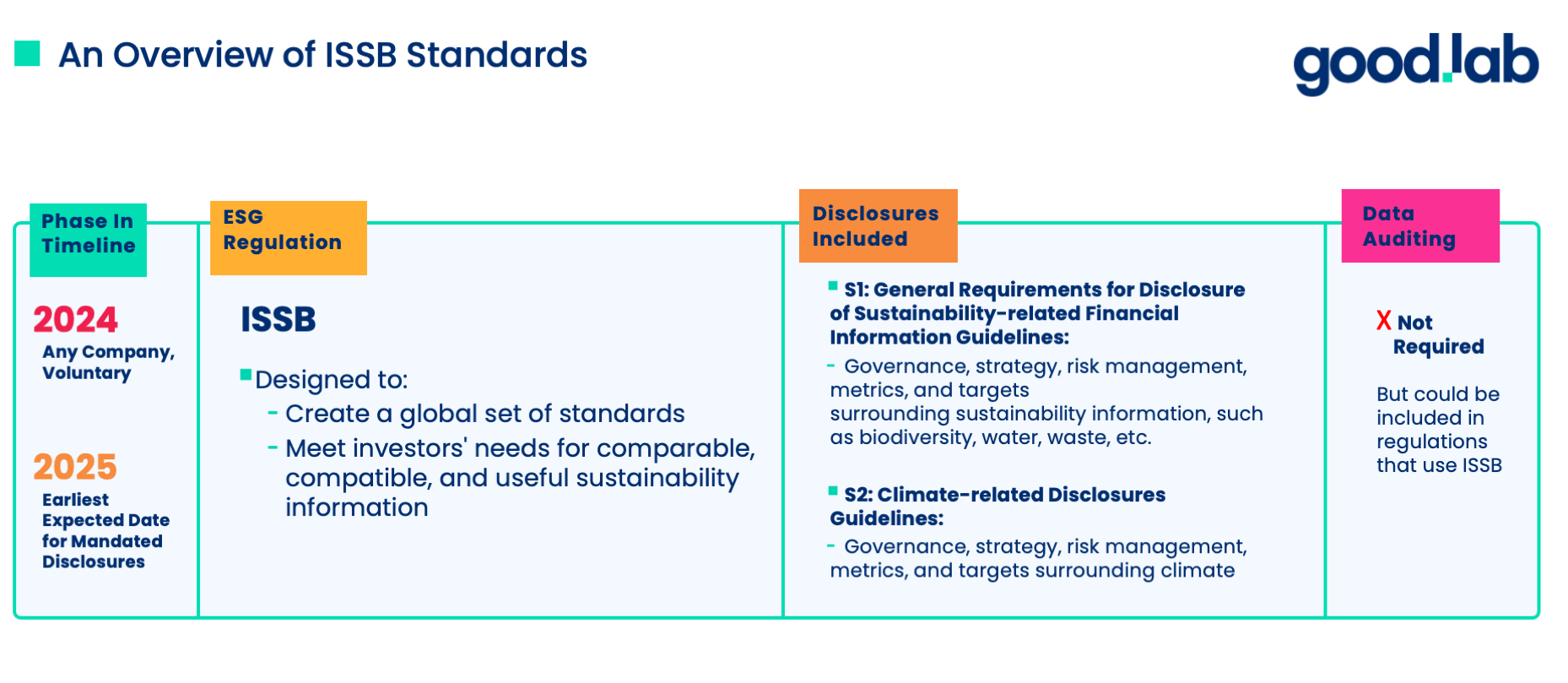

In 2025, companies can begin submitting their initial voluntary ISSB report for the fiscal year 2024. The ISSB expects only the disclosure of climate-related risks (excluding scope 3) in this initial year. The ISSB has granted a one-year grace period for the disclosure of overall sustainability-related data and scope 3 emissions.

ISSB Reporting Standards Disclosure Requirements

The ISSB’s first disclosure standards were based on the four reporting themes of the Task Force on Climate-Related Financial Disclosures (TCFD): governance, strategy, risk management, and metrics and targets.

The ISSB breaks out climate from general sustainability reporting because climate-related disclosures were considered the most important material issue for investors. However, the ISSB plans to break out the general sustainability standards into more specific criteria in the future.

S1 requires companies to report general sustainability-related information that could be reasonably expected to affect a company’s finances in the near, medium, or long term across the four themes of the TCFD:

Governance: The disclosure of the governance processes of how a company monitors, manages, and oversees sustainability-related risks and opportunities.

Strategy: The disclosure of how a company plans to manage its sustainability-related risks and opportunities.

Risk Management: The disclosure of the process of how companies identify, assess, prioritize, and monitor sustainability-related risks and opportunities.

Metrics and Targets: The disclosure of any sustainability targets and any operational or value chain sustainability metrics related to meeting these targets or relating to assessing the company’s performance in managing and mitigating sustainability-related risks and opportunities.

S2 requires companies to disclose their climate-related information that could be reasonably expected to affect a company’s finances in the near, medium, or long term across the four themes built by the TCFD:

Governance: The disclosure of how the governance processes of how these climate-related risks are monitored, managed, and overseen by the reporting company.

Strategy: The disclosure of information surrounding how they plan to manage their climate-related risks and opportunities.

Risk Management: Conduct scenario analysis and the disclosure of physical and transitional risks and opportunities across different climate scenarios.

Metrics and Targets: The disclosure of any climate target they have made and disclose the emissions across scope 1, 2, and 3 (scope 3 has a one-year relief period before disclosure is necessary) related to their climate risks and opportunities.

How Companies Can Prepare for ISSB Reporting

The ISSB standards will be widely adopted quickly in the next three years. Early adoption of these reporting standards will enable companies to get ahead of their competitors. Here are four steps to propel you into alignment with the ISSB standards:

Conduct a Materiality Assessment: The ISSB expects companies to report all material sustainability-related issues. They describe material issues as “if omitting, misstating or obscuring that information could reasonably be expected to influence decisions.” Therefore, conducting a materiality assessment will help you understand the extent of what you need to disclose. Materiality Assessments are an integral part of how we help companies set off on the right path as they build their ESG programming.

Assess Current Disclosures: If you currently report to one of the reporting frameworks or standards that will be integrated with the ISSB standards, such as the SASB, TCFD, or CDP, the ISSB advises you to continue reporting to them until 2024, as those disclosures will be applicable to much of the reporting under the ISSB. At Good.Lab, we have helped customers with every type of. We can help your company assess any required ESG disclosures you may be responsible for and any additions you may need to make to your disclosure for ISSB aligned reporting.

Start with Climate-related Disclosures: The 1-year relief period for general sustainability disclosures and scope 3 mean that companies should start the process by working out their governance, strategy, metrics and targets, and risk management around climate-related risks and opportunities and build out from there. Calculate your GHG emissions to get a handle on measuring and reporting your scope 1, 2, and 3 and consider how you will assess climate risks to build effective climate strategies.

Start Collecting ESG Data: Because ESG data resides in different areas of companies, creating winning strategies and governance practices for cross-functional engagement across finance, legal, ESG, and other teams is important for accurate and timely data collection and aggregation. Consider ESG software not just built for climate measuring and reporting, but also consider tools to help you record and report on every ESG metric material to your company.

Aligning your reporting to a new standard can be a difficult process, but the best advice is to just start!

Don’t Embark on your ISSB Compliance Journey Alone

The transition from companies using a diffuse set of ESG standards for reporting to using one across all jurisdictions and sectors is happening. When voluntary ISSB reporting begins in 2024, it is expected that many companies will quickly start using its standards.

We’ve been carefully tracking the evolution of the ISSB standards, and our team of ESG experts is on hand to guide your team on what it takes to report using the ISSB reporting standards and help you get started. From data collection to target setting to reporting, our ESG Software platform further simplifies the process. To get ahead of the game and not get left behind, reach out to Good.Lab to get started today!

Disclaimer: Good.Lab does not provide tax, legal, or accounting advice through this website. Our goal is to provide timely, research-informed material prepared by subject-matter experts and is for informational purposes only. All external references are linked directly in the text to trusted third-party sources.

Andries Verschelden

Co-founder & CEO

Andries has had a variety of consulting and management roles throughout his career. He has worked with fast-scaling clients across three continents. Prior to founding Good.Lab, Andries led the blockchain practice at Armanino, a top 20 public accounting firm, was CEO at The Brenner Group, a boutique Silicon Valley financial services firm, and was a partner at Moore Stephens in Shanghai. He started his career at PricewaterhouseCoopers.

Andries holds his B.S. in International Politics from Ghent University in Belgium, an MBA from Binghamton University and founded and participated in the Moore Comprehensive Executive Leadership Program at Harvard Business School.

Ready to elevate your sustainability efforts?

Connect with our sustainability experts today!

From sustainability program development to target setting, data management, and reporting, our team can help you fast-track building a world-class sustainability program.

Why the real AI risk has nothing to do with AGI Most conversations about AI risk focus on the future: superintelligence, mass unemployment, existential threats. That’s understandable and important, but it’s also a distraction. The most damaging AI failures companies face today have nothing to do with AGI. They are far more mundane, far more […]

The 7 Best CDP Consultants for Mid or Small-sized Companies in 2026

CDP disclosure is becoming the benchmark for measuring companies’ environmental performance and assessing supply chain risk. As the number of small- to medium-sized businesses (SMBs) being asked to make a CDP disclosure continues to grow, so does the competitive advantage of companies that respond. Working with the best CDP consultants can help your company maximize its environmental reporting and performance. However, each year, thousands of SMBs fail to respond, potentially missing opportunities to build […]

Whether your team has decided to hire an expert for CDP (formerly Carbon Disclosure Project) reporting or still weighing options, the next challenge is knowing how to evaluate potential support. Many organizations search for a CDP consultant or advisory partner with the hope of finding the right fit, but it is often less clear how […]

Welcome to Good.Lab! We're glad you're here and want you to know that we respect your privacy and your right to control how we collect and use your personal data. Please read our Privacy Policy to learn about our privacy practices or to exercise control over your data.