By January 1, 2026, more than 4,000 companies will be expected to report on their climate risks as part of California Climate Rule SB 261.

These reporters will be required to upload a TCFD-aligned climate risk report to the California Air Resources Board (CARB) public portal opened between December 1, 2025, and July 1, 2026. Companies will be required to post the location (URL) of their report on this docket by January 1 at the latest.

For many companies, this will be a net new process. And while in the first year they will avoid penalties if they make “good faith” efforts, those efforts will still require them to publish a TCFD-aligned report within the limits of what CARB considers good faith.

To help businesses prepare, we have reviewed 100 TCFD reports of companies that will likely be impacted by the California Climate Rules to identify best practices, provide guidance on what you should do to prepare, and illustrate what will ensure compliance with examples.

What is SB 261, and What Does It Require?

In 2026, California will become the first US regulator to implement a climate risk and emissions reporting mandate to companies doing business in its jurisdiction under SB 219.

One-half of those disclosures is SB 261, which will require companies doing business in California with more than $500 million in revenue to publish climate risk disclosures in line with the TCFD guidelines – or a similar framework (ISSB’s IFRS S2) – on January 1, 2026, and every two years thereafter.

Companies unable to fully comply must disclose available information, explain gaps, and outline plans to close them. In the first year of reporting, CARB has indicated that companies will avoid fines for “good faith” efforts. We’ll go into what that means throughout this guide.

What We Learned from Reading 100 TCFD-Aligned Reports on What it Will Take to be Compliant with SB 261

We used our own AI-assisted model that we use to benchmark TCFD reports for our clients to review 100 recent, public TCFD-aligned disclosures across sectors (manufacturing, transport, tech, consumer, financials, energy, and others) at companies that will likely be impacted by SB 261.

Five patterns stood out, and we share some deep dives into specific reports below:

- Companies substantively report on approximately six topics.

Although there are 11 topics, and every company mentions all 11, there was only substantive reporting on an average of 6 topics. - Governance is nearly universal. Financial linkage to climate risks lags.

Boards and management oversight are well-described in most reports, whereas quantified profit and loss impacts from climate risks and opportunities remain scarce. - Not many present a scenario analysis – and if they do, it tends to lack depth.

Most reports do not share climate risks under different warming scenarios such as Shared Socioeconomic Pathways (SSPs) and Representative Concentration Pathways (RCPs). - “Indexing” is the dominant format in some sectors.

“Indexing” is a format where companies create a table (an ‘Index’) that maps the TCFD framework’s four pillars to content they’ve already published in other sustainability or financial reporting. For very large public filers, this may be the fastest way to meet SB 261’s structure, as it points to the areas where they already comply with SB 261 without creating additional work. Alphabet, Target, Accenture, Keurig Dr Pepper, Campbell’s, and others all do this. - TCFD is already very common among large companies, and many mention ISSB’s S2.

Most large US filers still publish a TCFD report or index, sometimes alongside an ISSB S2 mention. There will likely be a transition period between the TCFD and ISSB, but most companies will likely eventually land on the ISSB. As the IFRS noted, “As the ISSB Standards start being applied around the world, the IFRS Foundation will take over responsibilities from the TCFD.”

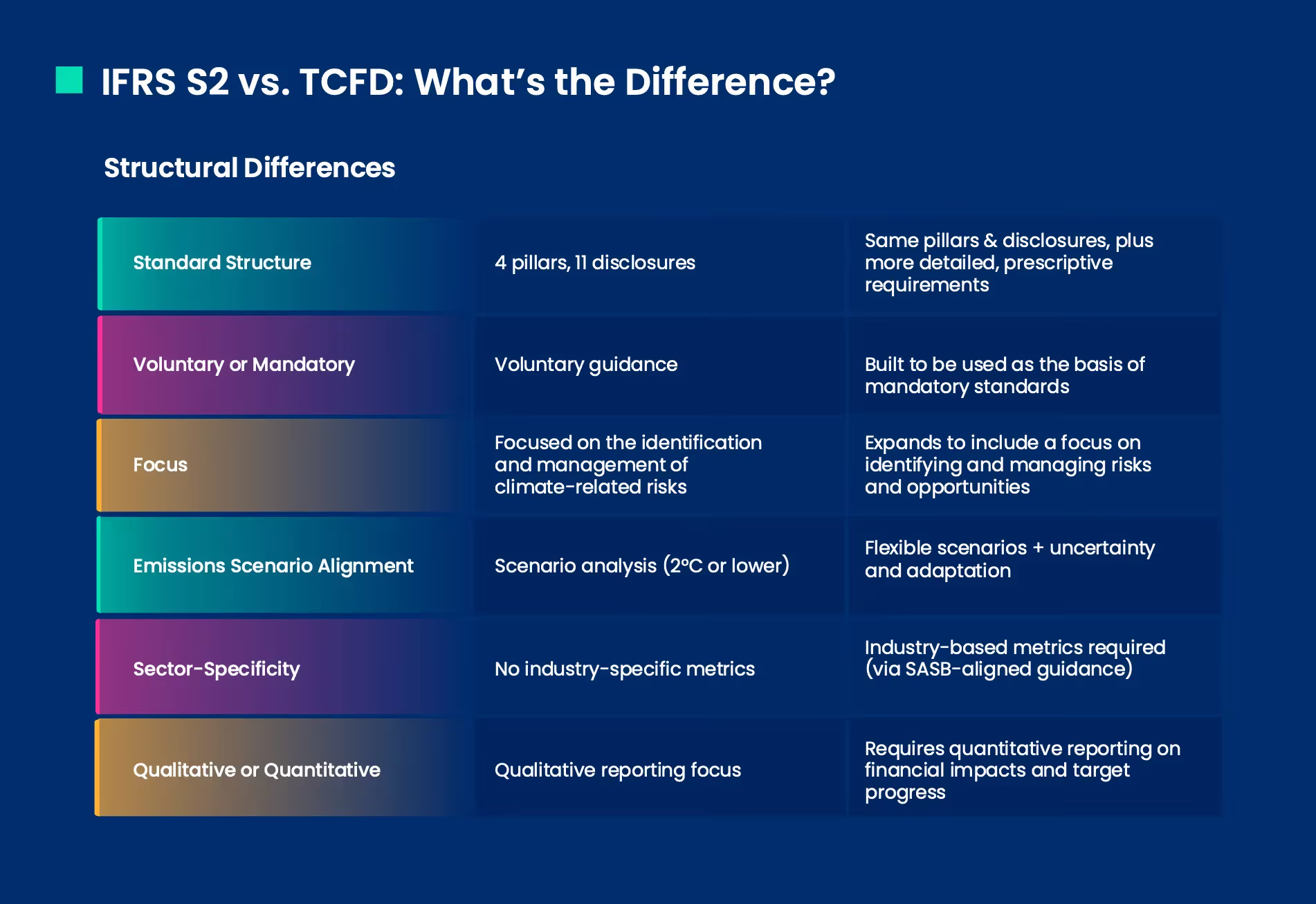

Here’s a closer look into the structural differences between TCFD and IFRS S2:

The bottom line is that you don’t need to disclose everything to be compliant in Year 1. As long as you have clear governance, a real risk process, strategy implications (even qualitative), and the measures you’re taking to reduce/adapt, you likely will have met CARB’s “good faith” effort requirement for this reporting cycle.

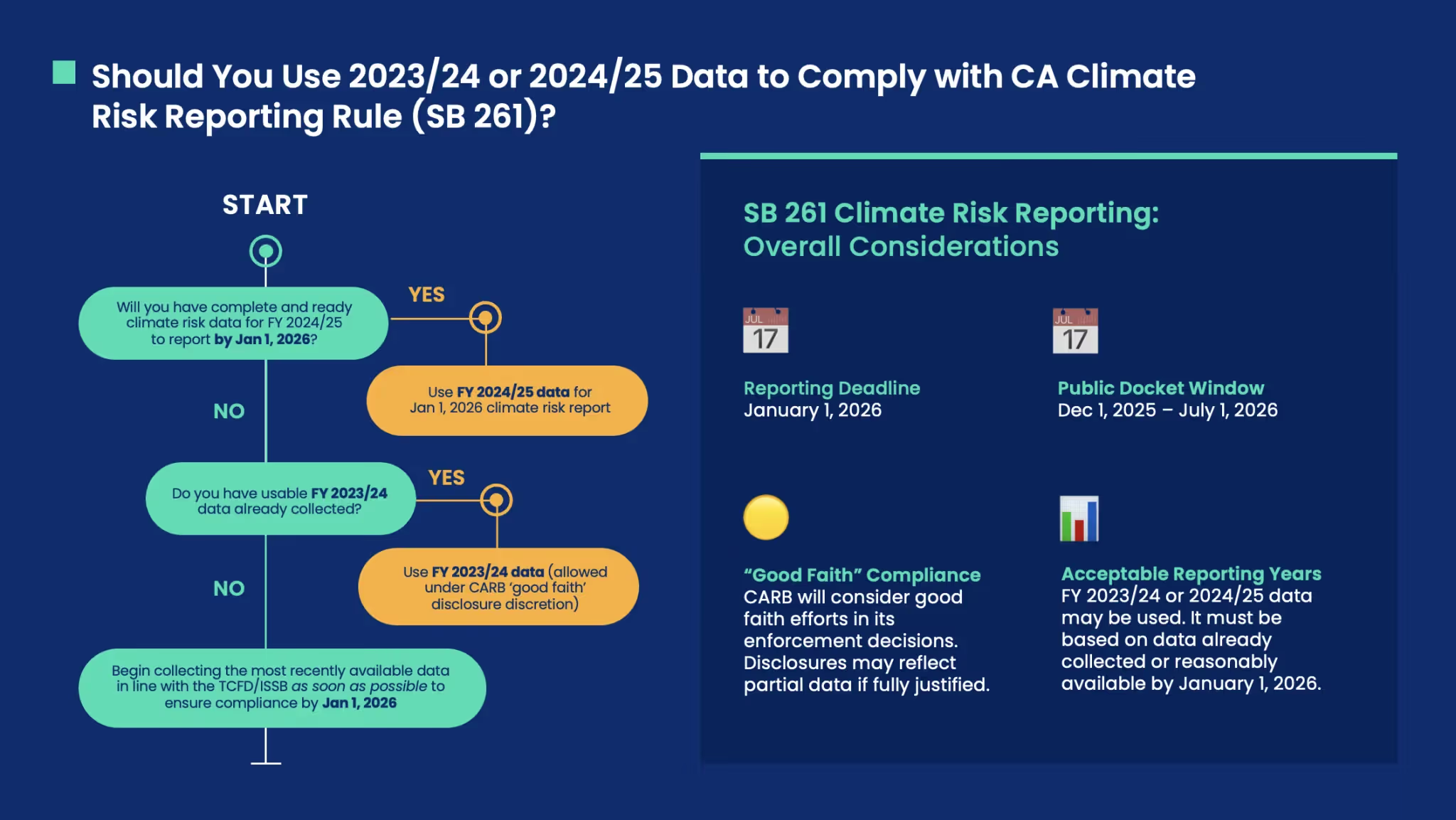

(Confused on whether to use FY 2023/2024 or FY 2024/2025 data for your "good faith" effort? Keep reading! We'll cover this with a simple flow chart right after industry differences.)

What A Good Climate Risk Disclosure Looks Like: Traits to Emulate for SB 261 Compliance

Out of the 100 TCFD-aligned reports we looked at in our research, we found that the average number of substantive disclosures was 5 topics higher than in other similar research (9 total, as opposed to an average of 4). This may be due to the smaller sample size and the fact that our sample was from more mature, larger companies.

Here is a snapshot of 8 of those companies to show what they are reporting to be in line with the TCFD.

- Rogers Corporation

Industry: Manufacturing & Materials

Topics Disclosed: 6

In its 2025 Sustainability Report Supplement, Rogers TCFD-aligned disclosures detailed its climate risk governance structures and its integration within Enterprise Risk Management. They also present their Scope 1 and 2 emissions metrics, an intensity measure, and a public target (20% reduction by 2030, base year 2022). It also introduces an in-progress climate risk assessment with scenario analysis planned for completion in 2025. - Enerpac Tool Group

Industry: Manufacturing

Topics Disclosed: 6

In its 2024 Sustainability Report, Enerpac provides a TCFD Index where it outlines the company’s board and management oversight of climate matters, identifies demand- and weather-related risks, and highlights opportunities in clean energy and electrification markets. It discusses impacts on strategy and references business resilience planning. Enerpac also describes enterprise-level risk management integration. However, the company does not publicly disclose carbon emissions, does not provide scenario analysis, and lacks externally communicated climate-related targets. - Whirlpool

Industry: Manufacturing

Topics Disclosed: 8

In its 2024 Sustainability Report, Whirlpool provides a dedicated TCFD Index where it identifies climate-related risks and opportunities using scenario analysis, outlines governance structures including board-level oversight, and sets climate goals such as net-zero for Scope 1 and 2 emissions by 2030. However, Whirlpool lacks in the strategy topic and for addressing the financial impacts of climate risks topics. - Johnson Controls

Industry: Automotive Manufacturing

Topics Disclosed: 9

In its 2024 Sustainability Report and dedicated TCFD index, Johnson Controls discloses its governance practices. The strategy topic reporting integrates climate-related risks and opportunities into enterprise risk management and is supported by scenario analysis. Metrics and targets include Scope 1, 2, and 3 emissions, science-based interim targets, and a net-zero 2040 goal. However, financial impacts and long-term resilience analysis are less developed. - Mondelēz International

Industry: Food & Beverage

Topics Disclosed: 10

In its 2024 Snacking Made Right report, ESG Datasheet, Proxy Statement, and CDP Climate responses, Mondelēz outlines climate-related governance, risk management, and sustainability strategies. It provides a detailed TCFD index mapping disclosures to the 11 recommended areas for 2024 but is lacking in some resilience strategy responses. - Howmet Aerospace

Industry: Aerospace & Defense

Topics Disclosed: 11

In its 2025 TCFD Disclosure, Howmet delivers substantive, decision-useful reporting across all 11 TCFD areas. Governance is well integrated, with a strategy that includes quantified risk and opportunity analyses and scenario analysis tested across different climate pathways. Risk management is embedded in enterprise risk management, and metrics and targets are robust, featuring externally assured GHG data, intensity measures, and climate targets over the short and long term. - Gilead

Industry: Biopharmaceutical

Topics Disclosed: 11

In its 2024 report, Gilead has integrated climate considerations into its business strategy by setting robust decarbonization commitments, conducting scenario analyses of physical and transition risks, and publishing disclosure across all 11 TCFD topics. - Chubb

Industry: Insurance

Topic Disclosed: 11

Chubb’s fourth annual TCFD report outlines its science-based insurance approach to climate change. The company has a very mature approach to reporting aligned with the TCFD’s 11 topics, with Scope 1, 2, and 3 metrics reporting a net zero target. Chubb has a robust governance structure around climate risks and a well-developed structure for climate risk and opportunity assessments and strategies.

Throughout this exercise, we found that companies that are more mature in their TCFD reporting, having reported consecutively for multiple years, are more likely to have more topics disclosed. Also, we found that the sectors identified in the ISSB’s progress report as reporting on more elements, like insurance and pharma, tend to report on more topics.

Map SB 261 To What You Actually Need to Publish in Year 1

If you are preparing for your first climate risk disclosure in line with the TCFD, the key thing to remember is that you only need to report on material elements of the 11 TCFD reporting topics – topics that are likely to have a financial impact on the company.

What we found in our research of 100 TCFD reports is supported by the conclusions of the 2024 ISSB progress report, which also includes progress on TCFD (as the ISSB took over the responsibilities of the TCFD in 2023), indicating that US companies make substantive disclosures on 4 of the TCFD’s 11 disclosure topics on average, meaning many of the topics are not as material and don’t need substantive coverage. This number was slightly lower than our average, likely due to the much larger sample size and maturity range.

The focus of those 4 average topics surrounds board oversight, GHG emissions, and the assessment of risks and opportunities (similar to our study), all of which more than half reported to, as seen in the table below.

Disclosure by Region for FY 2023: North America

Reporting Pillar Reporting Topic Average % of North American Companies Reporting Governance Board oversight 59% Management’s role 38% Strategy Risks and opportunities 53% Impacts of risks and opportunities on company 31% Resilience of strategy 8% Risk management Risk identification and assessment process 25% Risk management processes 29% Integration into overall risk management 20% Metrics and targets Climate-related metrics 42% GHG emissions 52% Climate-related targets 49%

The report also found that very few companies are undertaking the more complex parts of TCFD reporting, with only 8% of companies doing scenario analysis.

We expect that if companies can provide substantive reports on at least four to six material topics, as is the case in both the ISSB progress report and out own research focusing on governance of board oversight, the assessment of climate risks, and targets, you will be able to explain gaps and outline plans to close them easily, thus ensuring compliance with SB 261.

CARB confirmed that a scenario analysis and GHG emissions will not be required to share for SB 261 compliance. For January 1, 2026, a company may instead have a qualitative discussion in its SB 261 report.

How Climate Risk Disclosure Varies by Industry

While SB 261 does not require sector-specific data, each company will have different material risks and opportunities, and more mature companies and sectors may choose to disclose more.

The 2024 ISSB progress report found that some sectors reported against more TCFD elements than others:

- 6 or more elements: Energy, Insurance, Manufacturing

- 3-5 elements: Pharma, Retail, Tech

- 3 or fewer elements: Consumer Packaged Goods, Financial Firms

It is worth considering that if you are an energy company, good faith reporting to comply with SB 261 might look different than if you are a consumer goods company.

"Good Faith" Effort: What’s 'Enough’ for the First TCFD-Aligned January 1, 2026 Report?

CARB has made it clear that in year 1 of climate risk reporting under SB 219 (SB 261 + SB 253), they don’t expect companies to get it perfect. They will allow "good faith" efforts.

Under these good faith efforts, companies will still be expected to identify and assess climate risks and opportunities and report them in line with the requirements, and it must be submitted on the submission platform by January 1, 2026. However, companies can use a “report or explain” policy in this first year, where they report on what topics they can, and explain why they cannot report on others.

Should I Use FY 2023/2024 or 2024/2025 to Comply with CA SB 261?

Good.Lab’s 5 Steps to SB 261 Compliance

At Good.Lab, we’ve refined our process through working with dozens of clients to get them prepared for compliance with SB 261. Here’s how our Climate Regulation Solution guides you from start to finish:

1. Assess – We start with a rapid diagnostic against the four TCFD pillars: Governance, Strategy, Risk Management, and Metrics & Targets. A brief survey and interviews with up to five team members identify gaps in policy, data, and oversight. You get a quantified readiness scorecard on day one.

2. Benchmark – Using our AI-powered research engine, we scan peer disclosures, TCFD filings, CDP responses, and annual reports, so you can see exactly where leaders in your sector are setting the bar. The result: a maturity range that shows what “minimum compliance” looks like versus “industry leading.” As shown above, some sectors report against many more topics than others. Knowing what your competitors are doing ensures there are no discrepancies when it comes to disclosure.

3. Roadmap – With your assessment score and benchmark range in hand, we create a prioritized action plan. Each gap becomes a clear, assignable, time-bound task. A working session with your team locks in ownership and deadlines, so progress begins immediately.

4. Outline – Before drafting, we hold a calibration workshop to define the scope and ambition of your report. Whether your goal is simple compliance or a high-visibility leadership position, the outline specifies narrative themes, required metrics, and supporting evidence.

5. Publish – We prepare a concise, five-page TCFD-aligned report tailored to California’s submission portal (and any future CARB formatting rules). We also package all underlying worksheets and guide your team through the upload process.

We’ve worked with companies at all stages of TCFD maturity. Whether you're just starting or revising a first draft, our advice is the same: Be transparent, be specific, and don’t wait for perfect data to get started.

After January 1, 2026, you will have until January 1, 2028 to refine your processes and ensure compliance with future stricter requirements for avoiding penalties.

Beyond SB 261 reporting, Good.Lab can help with every aspect of climate reporting, including GHG emissions calculations in line with SB 253, target-setting, climate risk assessments, and CDP filings – so you can move beyond compliance and turn climate action into a competitive advantage.

Ready to get moving on California compliance? Talk to Good.Lab’s subject matter experts ➔